In the delicate balance of family and finance, trust often becomes the most fragile currency. When the sister-in-law reached out for a short-term loan, a simple request morphed into a test of boundaries and principles. The lender, striving to protect both heart and wallet, proposed terms designed to safeguard fairness and clarity—only to be met with resistance and wounded pride.

Beneath the surface of dollars and contracts lies a deeper struggle: the fear of betrayal and the pain of misunderstanding. What began as an offer of support twisted into a silent standoff, revealing how even generosity can be shadowed by doubt, and how love sometimes demands the hardest negotiations.

AITA: Family member loan – I asked for an agreement

According to financial planning experts like Suze Orman, lending money to family members is inherently risky because it mixes emotional relationships with legal obligations. Orman strongly advises that if one chooses to lend, the terms must be written down, regardless of how close the relationship is, to prevent miscommunication and resentment later.

The narrator’s motivation stems from a desire for boundary maintenance and risk mitigation, evidenced by their history of witnessing family loan disasters. Offering favorable terms (six months interest-free, 15-year amortization) demonstrates a willingness to help substantially. However, the sister-in-law’s reaction—refusing the contract and framing the interest as ‘making money’—suggests a fundamental mismatch in expectations regarding the nature of the transaction. The sister-in-law viewed it as an unconditional favor, while the narrator viewed it as a formal, albeit generous, loan.

The secondary issue involves communication; the sister-in-law relayed her negative perception to the narrator’s wife, bypassing direct communication, which introduces unnecessary strain on the marriage. While the narrator’s request for documentation is financially prudent and appropriate for sums over $1000, future handling should involve preemptive discussion about documentation before terms are even offered. If the narrator is truly unwilling to accept any interest, they should present the contract as a formality protecting the repayment timeline, rather than a profit-seeking measure, or simply convert the loan to a gift if the amount is small enough to avoid future conflict.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

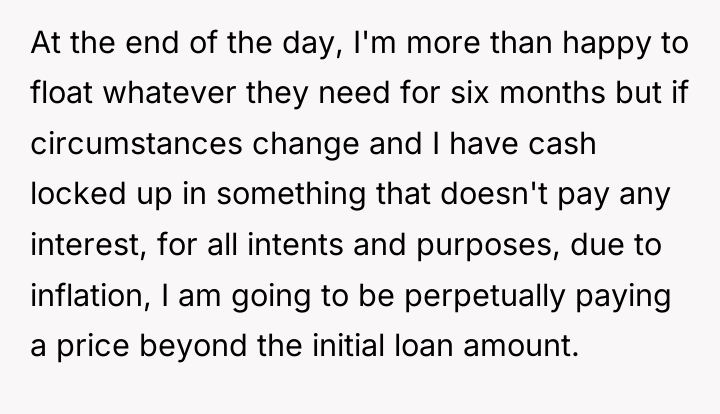

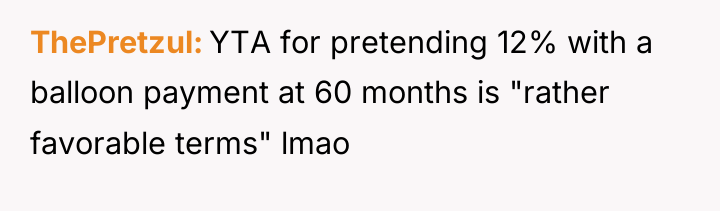

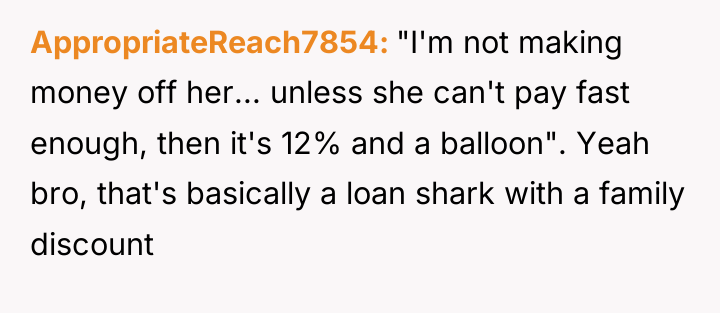

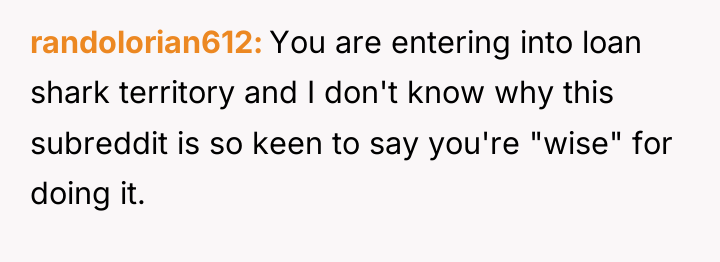

With 12% interest kicking in after the initial six months, you *are* setting yourself up to “make money off of her” if she has any sort of problem getting the debt repaid in the next 6 months – illness, accident, job loss, etc.

N-T-A for wanting a formal agreement, but YTA for the overly punishing terms.

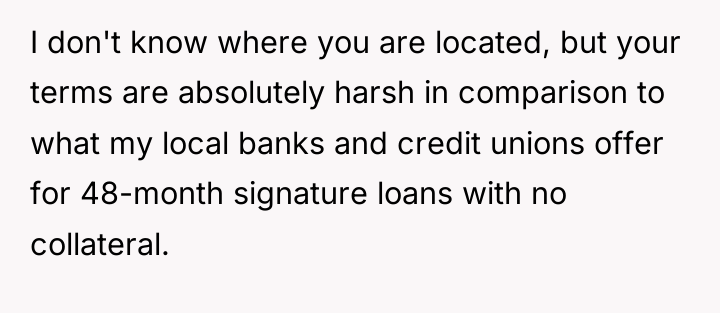

The terms are favorable to you for sure, but you know they’re truly dogshit for her when they’re worse than even what credit card debt consolidation places typically offer (8-11% and no balloon payments).

The individual faced a direct conflict between their established personal boundary—requiring a contract for larger loans to protect relationships—and the sister-in-law’s expectation of an immediate, informal cash transfer based purely on trust.

Is prioritizing clear, documented financial agreements over immediate familial accommodation a necessary step for maintaining healthy boundaries, or does insisting on formal terms undermine the trust inherent in close family lending?

{kind=link}