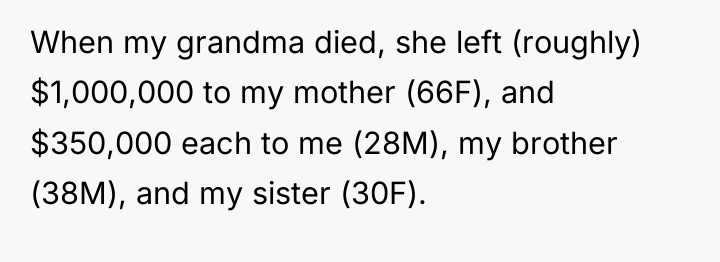

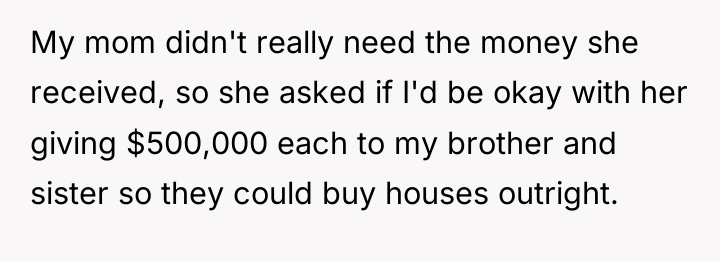

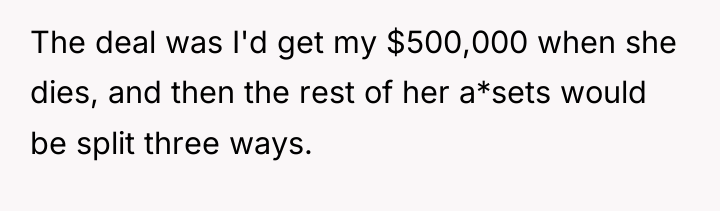

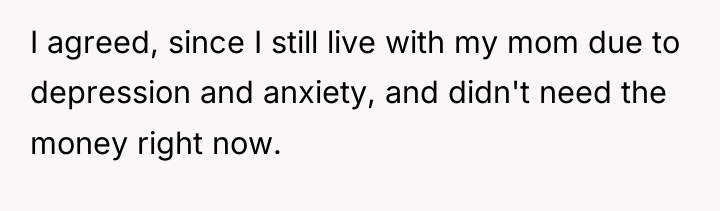

In the quiet aftermath of their grandmother’s passing, a family found themselves weaving a complex tapestry of love, trust, and financial legacy. What began as a generous bequest soon became a delicate negotiation, revealing not just the value of money, but the fragile bonds that hold them together.

Amidst the shadows of anxiety and the promise of future security, one son grappled with the weight of time and inflation, seeking fairness in a shifting landscape. His mother’s willingness to adjust her will became more than a legal act—it was a testament to understanding, sacrifice, and the enduring hope for balance in the face of life’s uncertainties.

AITA for expecting my delayed inheritance to be adjusted for inflation?

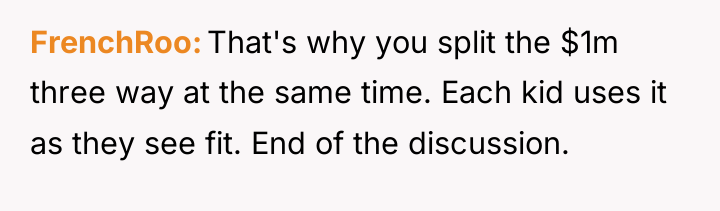

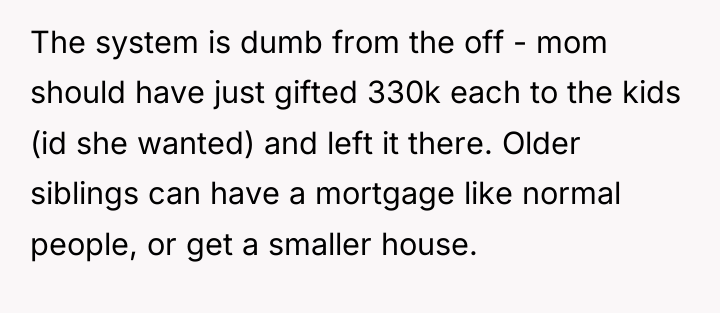

According to family finance experts like those often cited in wealth management literature, agreements made regarding estate distribution, even informally among close family, carry significant emotional weight and should prioritize clear, written documentation to prevent future misunderstandings. The core issue here involves concepts of equity versus equality. While the initial distribution aimed for equality (giving siblings an immediate asset—a house), the OP’s delayed receipt introduced an element of financial inequality that inflation adjustment sought to correct, aiming for true equity based on purchasing power.

The brother’s reaction stems from perceiving the OP’s situation (living at home, investing existing funds) as inherently privileged compared to their own need to immediately purchase housing. This perception of unfair advantage fuels resentment. His argument that the OP’s investment gains negate the need for inflation protection ignores the fundamental difference between realized investment profit and the guaranteed erosion of cash value over time. The mother acted reasonably by agreeing to the inflation adjustment initially, recognizing the time value of money.

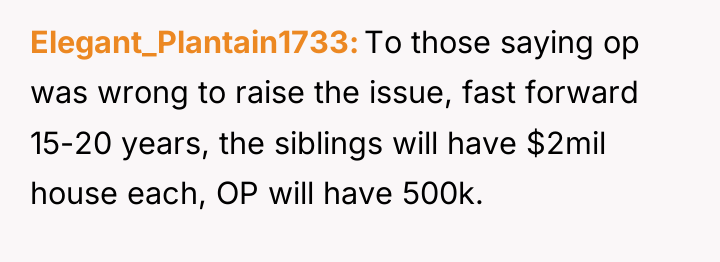

The OP’s decision to revert the agreement simply to prevent an argument is understandable given anxiety and a desire to maintain peace, but it sets a difficult precedent. A more constructive approach would involve open communication, perhaps offering the siblings a transparent explanation that the investment growth and the inflation adjustment are separate issues. In future situations involving deferred wealth transfer, all parties should formally agree on how inflation, investment performance, and current living situations will be factored into the final distribution plan before any money or property changes hands.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

![[deleted] ESH. You're all arguing over money you get when...](https://animalstrend.com/wp-content/uploads/wp-img-cache/a864b24952a66befa085174f74f308a2.png)

![[deleted] Obviously y'all are rich. But not enough that your...](https://animalstrend.com/wp-content/uploads/wp-img-cache/b7795203c1e9d2064e83e0fcd6e8b9e7.png)

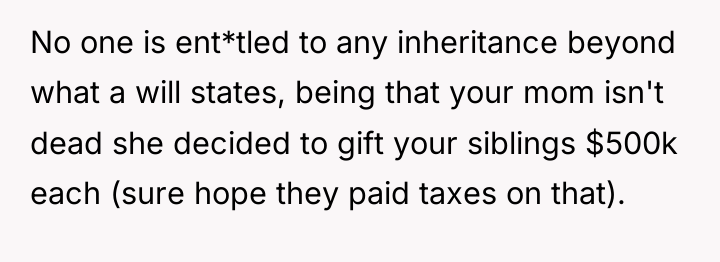

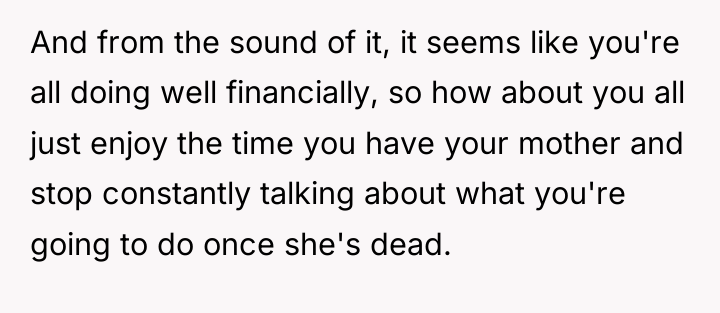

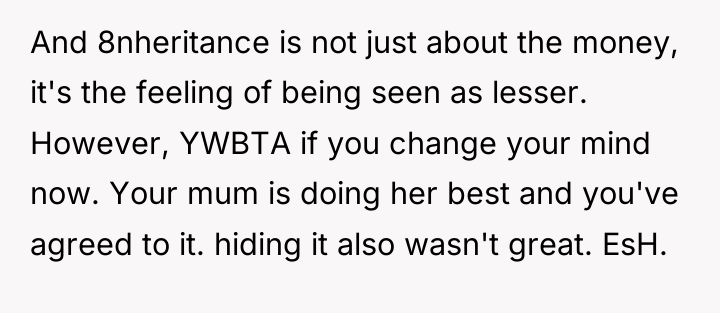

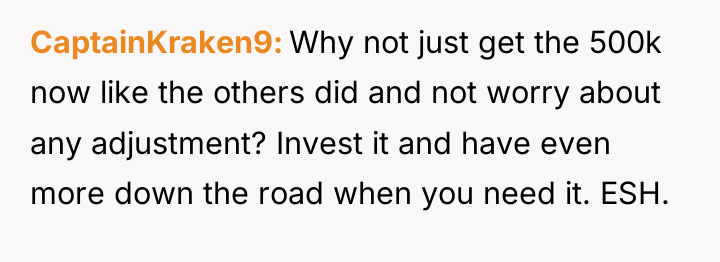

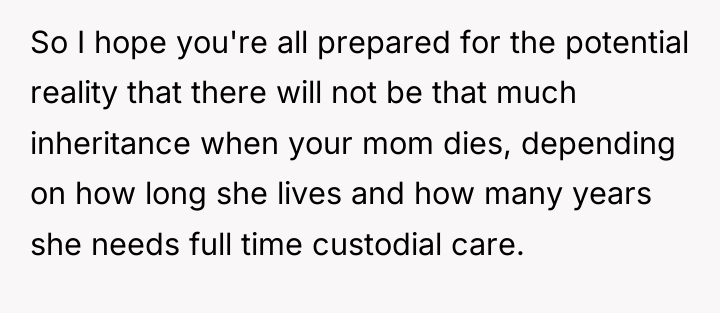

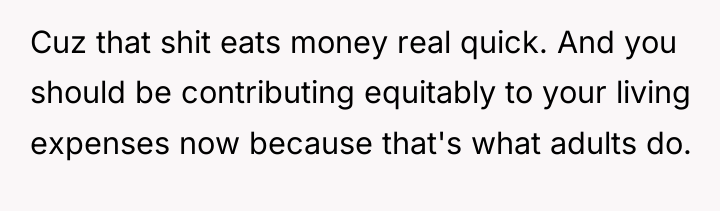

The individual felt their request to adjust the inheritance amount for inflation was fair, especially given the delay in receiving the funds. However, they ultimately conceded to their brother’s demands to avoid conflict, suggesting a prioritization of family harmony over asserting their perceived financial right.

Was the decision to reverse the inflation adjustment the right choice to preserve family peace, or did it unjustly sacrifice a reasonable financial expectation? Should the value of an inheritance promised for the future be fixed in today’s terms, or should the recipient accept the nominal amount regardless of economic changes?

{kind=link}