In the quiet corners of a European life shaped by social safety nets and cultural contrasts, one woman grapples with the delicate balance of family, finance, and perception. Her story unfolds not as an accusation, but as a heartfelt reflection, revealing the complexities behind the scenes of everyday struggles and the unseen layers of partnership.

Amidst the backdrop of public healthcare and affordable childcare, she confronts the realities of budgeting and the subtle tensions that arise when personal views and societal norms collide. Her journey is a testament to the resilience found in reassessment and the courage to share a narrative that is both personal and universally human.

AITA for refusing to pay my half of a loan I took together with my husband?

The situation described touches upon core concepts in relationship psychology concerning financial fusion versus financial autonomy. As noted by financial therapist and author Dr. Brad Klontz, founder of the Financial Therapy Association, ‘Money scripts—the stories we learned about money from our families—drive our financial behaviors, often unconsciously.’ In this case, the poster exhibited a strong ‘money script’ favoring separate accounts, common in modern European contexts where robust social safety nets reduce the perceived need for total financial fusion.

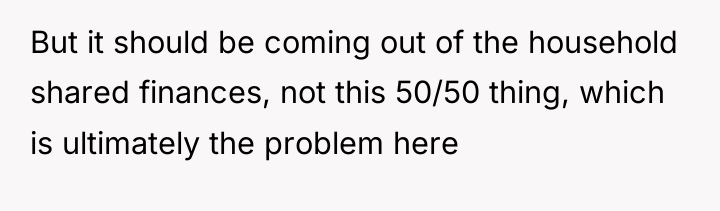

The conflict arose because the poster’s cultural norm (separate accounts with intuitive sharing) clashed with the husband’s presumed norm (a unified budget or a different splitting method). The initial disagreement was less about the absolute amount of money and more about the underlying principles of partnership: control, transparency, and perceived fairness. The cultural context provided by the poster—strong social welfare and the commonality of separate accounts—validates the poster’s initial stance as standard practice in their environment, yet it did not solve the interpersonal negotiation.

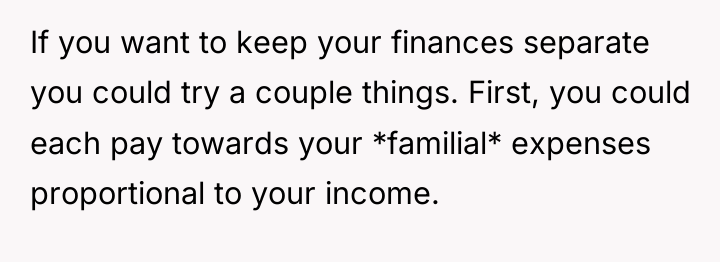

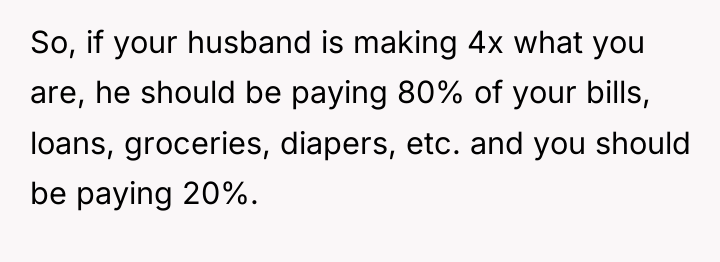

The final agreement to split expenses proportional to income is a mature compromise, blending the need for fairness (proportionality) with the need for structure (a set system). This approach acknowledges different earning capacities while ensuring both partners contribute equally relative to their means. The constructive recommendation is for the couple to clearly document this new agreement in writing, setting a review date (e.g., annually) to ensure the system remains equitable as incomes change, thereby preventing future misunderstandings rooted in unstated assumptions.

AFTER THIS STORY DROPPED, REDDIT WENT INTO MELTDOWN MODE – CHECK OUT WHAT PEOPLE SAID.

![[deleted] [deleted]](https://animalstrend.com/wp-content/uploads/wp-img-cache/dab68815e741901b5aa32b50799977a4.png)

![[deleted] You took out the loan together, you pay for...](https://animalstrend.com/wp-content/uploads/wp-img-cache/6252cd667cae8030dfed9533b51fa051.png)

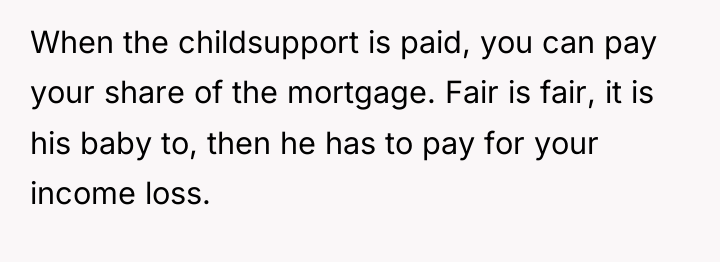

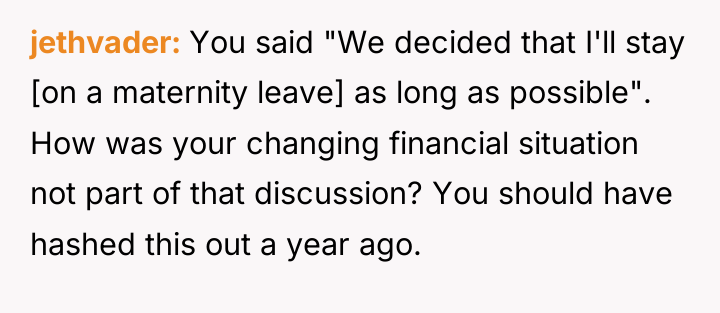

The original poster found value in the community feedback, leading to a deeper understanding of financial expectations and cultural differences regarding shared money management within a marriage. The central tension revolved around the poster’s expectation of separate financial autonomy versus the traditional view of a unified marital budget.

Given that the couple has decided to implement an income-percentage-based split for all bills, including the loan payment, the main question remains: Will this structured, proportional approach successfully balance individual financial autonomy with the shared responsibility required for long-term marital security?

{kind=link}