A young graduate, fueled by hope and gratitude, once relied on his father’s promise to support his education without expecting repayment. The silent pact was simple: dad pays tuition, the son chases dreams, and someday, he would pay it forward. But life’s debts often come with unexpected prices, and what began as unconditional love soon tangled in the heavy weight of unspoken expectations.

Years later, when the father asked for a large loan, the son’s world shifted beneath his feet. Torn between loyalty and self-preservation, he lent the money, swayed by the memory of past sacrifices and a sense of obligation. Yet as time stretched on without repayment, the lines between love, duty, and resentment blurred, leaving him to question the true cost of family promises.

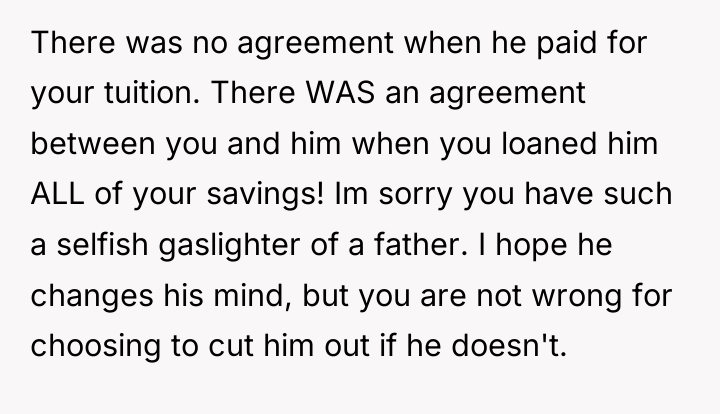

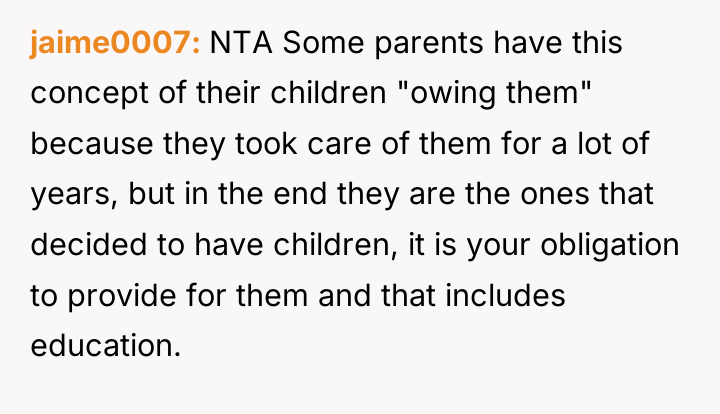

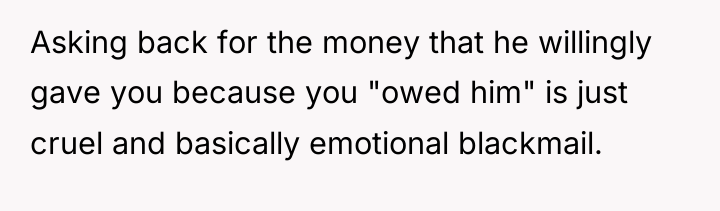

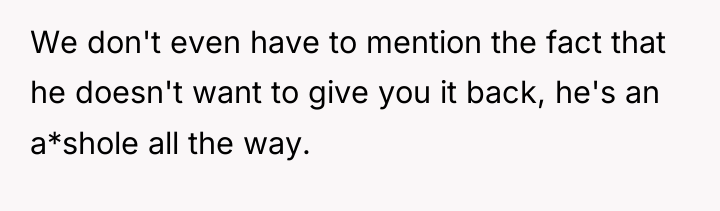

AITA for not speaking to my dad after he refused to pay back the $40k I loaned him because he paid for my college tuition years prior?

Dr. Terri Givens, an expert in family dynamics and finance, often notes that financial transactions between parents and adult children are fraught because they blur the lines between gift, investment, and loan. The core issue here is the lack of explicit communication and documentation, which allowed the father to unilaterally redefine the nature of the debt.

The father’s actions demonstrate a significant boundary violation and a misuse of parental leverage. By initially framing college tuition as an unstated gift or investment in the child’s future, and then later weaponizing it to negate a separate, substantial loan, he engaged in emotional manipulation. The adult child felt obligated because the father introduced the tuition repayment condition *after* the fact, exploiting the existing power differential and the child’s genuine sense of gratitude. This behavior shifts responsibility and denies the adult child’s financial autonomy.

The adult child’s expectation of repayment for the $40,000 was entirely reasonable; a transfer of this magnitude, regardless of past favors, legally and ethically constitutes a loan unless explicitly stated otherwise beforehand. Moving forward, the best practice in such situations is to always define financial agreements in writing, clearly stating whether a transfer is a gift, an investment, or a loan with defined repayment terms. This protects both parties and preserves the relationship by establishing clear, mutual expectations.

THE COMMENTS SECTION WENT WILD – REDDIT HAD *A LOT* TO SAY ABOUT THIS ONE.

Wow your dad is a piece of work. He pays for his childs tuition then uses that years later to manipulate you into giving him money, then LIES to you and now won’t help his struggling son?!

He literally called it a loan and once he got the money he switched on you and said he was keeping it because you owed him.

The individual felt trapped between a sense of obligation stemming from past parental financial support (college tuition) and the clear breach of trust when a later, explicit loan was effectively recast as repayment. This created a significant internal conflict where established familial expectations clashed with the reality of financial agreements.

Given that the father retroactively redefined the terms of the later loan by invoking the tuition as payment, was the adult child entirely unreasonable in expecting repayment for the $40,000 they willingly loaned, or does the initial investment in education outweigh the need for explicit contractual clarity in family finance?

{kind=link}