Caught between the weight of family loyalty and the fragile promise of their own future, they face a heart-wrenching dilemma. Their mother’s plea to take out a loan for the family’s mortgage deposit is wrapped in hope and desperation, but beneath it lies a fear of being left financially stranded. The burden of debt is no stranger to their parents, and the risk now threatens to fall squarely on their shoulders.

At the crossroads of independence and obligation, they grapple with the harsh reality of limited resources and uncertain repayment. Just stepping into college and leaving behind full-time work, their carefully saved funds are meant for education and security. Yet, the yearning to move forward—to create space for themselves amid a crowded household—pulls them toward a choice that could define their future in ways they cannot yet foresee.

My parents want me (19f) to take out a loan to help with their mortgage

Dr. Terri Givens, a specialist in financial psychology and family dynamics, often emphasizes the importance of clear financial boundaries in familial relationships. She notes that when financial support involves taking on direct legal liability, the relationship shifts from one of mutual support to one of creditor and debtor, which can severely strain trust.

The situation involves significant psychological pressure stemming from the living arrangement. Living rent-free creates an implied sense of obligation, which the parents appear to be leveraging, consciously or not. The conflict is multi-layered: the OP needs space for online college work, which directly impacts their academic success, while the parents’ request taps into the OP’s desire to maintain family harmony. The OP’s concern about being left ‘on the hook’ is highly rational given the parents’ existing debt and history of unreliable financial management. Taking out a loan as an accommodation, even with a verbal promise of repayment, transfers 100% of the legal risk onto the OP.

The OP’s proposed action (taking the loan) is inappropriate because it exposes their critical educational funds to undue risk based on an unreliable repayment history. A constructive recommendation would be to refuse the loan application directly but offer an alternative form of financial assistance that does not involve taking on debt. This could include gifting a smaller, manageable amount from current savings, or restructuring their living situation by helping to find a more affordable shared housing arrangement for the whole family, rather than taking on a debt the parents cannot legally assume.

THIS STORY SHOOK THE INTERNET – AND REDDITORS DIDN’T HOLD BACK.

They have options.

![[deleted] [deleted]](https://animalstrend.com/wp-content/uploads/wp-img-cache/dab68815e741901b5aa32b50799977a4.png)

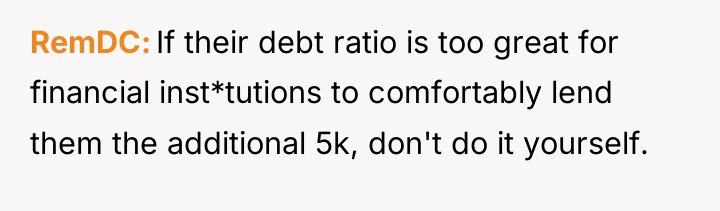

![[deleted] Under no circumstances should you ever do this.](https://animalstrend.com/wp-content/uploads/wp-img-cache/fb7178805f8263773cd478d4be887387.png)

The individual is facing a difficult choice between supporting their parents’ significant financial goal of buying a home and protecting their own limited savings meant for education and future independence. The core conflict lies in the parent’s request for a loan taken out by the child, despite a history of inconsistent repayments from the parents.

Should the individual prioritize their financial security and educational needs by refusing to take on debt for their parents, or does their current debt-free living situation obligate them to assist their family in achieving homeownership, even with the risk of default?

{kind=link}