Years ago, a mother quietly began weaving a hopeful future for her son, setting aside small but steady savings amidst the everyday struggles of life. Each $25 deposit, every modest tax return contribution, was a labor of love—an unspoken promise to protect and nurture her child’s dreams, even when circumstances demanded sacrifice and patience.

But the fragile balance of trust she built has been shaken by her mother-in-law’s insistence to intrude, threatening to unravel the careful boundaries she set. What started as a sanctuary for their son’s future now faces the tension of control and respect, as the mother fights to keep her son’s savings—and their family’s intentions—safe from forces beyond her control.

AITAH for refusing to give out my son’s saving account information?

According to financial educator Tiffany Aliche, clear boundaries and open communication are essential when managing family financial expectations. In this situation, the mother is establishing a necessary boundary to protect her child’s financial future and sensitive bank details. Giving out account routing and transit numbers to extended family members, even with good intentions, introduces unnecessary security risks and complicates account management.

The conflict highlights underlying power dynamics and differing expectations within the family. The mother-in-law likely views direct access as a sign of trust and a way to feel closely connected to her grandchild’s future. By rejecting this request, the mother’s actions may be interpreted by the mother-in-law as a lack of trust, leading to the current silent treatment. However, the mother has offered reasonable alternatives, showing she does not want to prevent the grandmother from contributing, but rather wishes to maintain control over her child’s financial privacy.

The mother’s decision to keep the savings account private is appropriate. To resolve the tension, she should initiate a calm, direct conversation with her mother-in-law. She can reassure the grandmother of her valued role in the child’s life while gently explaining that financial privacy is a strict rule they apply to everyone. Offering a joint visit to the bank to set up a secure direct-deposit method that does not expose full account details could also serve as a practical compromise.

THIS STORY SHOOK THE INTERNET – AND REDDITORS DIDN’T HOLD BACK.

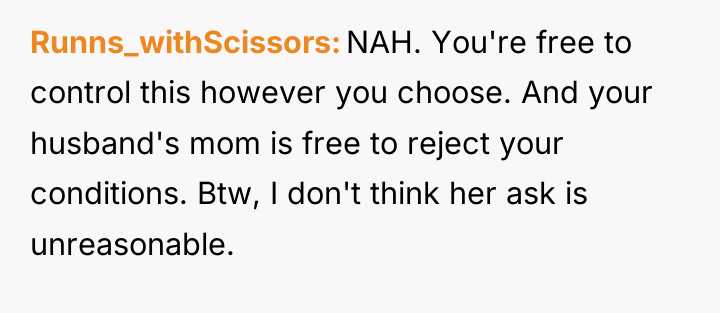

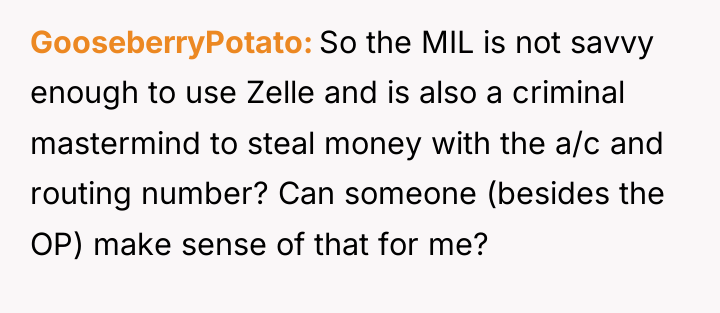

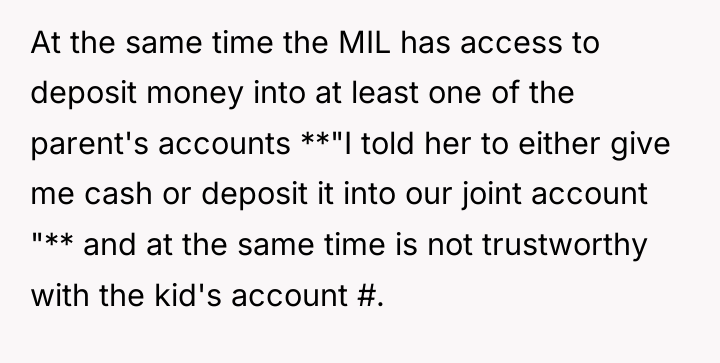

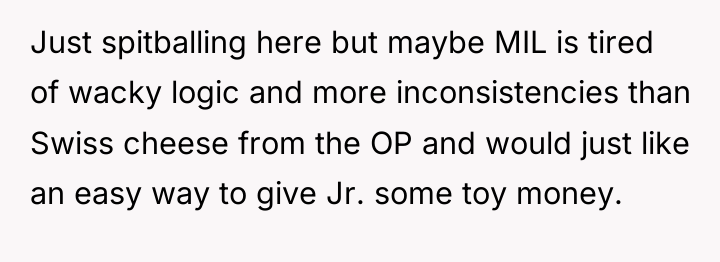

I don’t understand:

Why is it a problem to give her the information? Do you fear she will withdraw from the account or wants to know how much the balance is?

The mother feels highly protective of her son’s financial security, believing that restricting access to the savings account is her parental duty. However, this boundary clashes directly with her mother-in-law’s desire for direct involvement in her financial gifts, leading to silence and strained family relationships.

Was the mother right to stand firm on her strict security boundaries to protect her son’s account, or is she being unnecessarily defensive and hurting family harmony by rejecting a grandmother’s direct involvement?

{kind=link}