She stands at a crossroads, torn between love and financial independence, grappling with the heavy weight of a decision that could redefine their future. Moving from the bustle of a large city to the quiet hum of a smaller town, she seeks stability and a place to call her own, even as her boyfriend hesitates to fully commit to their shared life.

Caught in the storm of a brutal housing market and conflicting expectations, she faces not just a purchase, but a test of trust and partnership. His refusal to contribute without formal recognition on the mortgage threatens to unravel their plans, exposing the fragile balance between love, security, and the reality of building a home together.

AITA for not putting my boyfriend’s name on the mortgage?

According to personal finance expert Ramit Sethi, author of I Will Teach You To Be Rich, mixing pre-marital finances with major property purchases without clear legal boundaries is a significant financial risk. Sethi emphasizes that couples must have honest, structured conversations about money, equity, and expectations before making long-term commitments like buying a home together. In this case, the lack of a shared financial plan is creating unnecessary tension.

The conflict stems from mismatched expectations and a lack of clear boundaries regarding property ownership. The boyfriend’s refusal to pay rent unless his name is on the mortgage represents a power struggle. From a financial perspective, putting a non-contributing partner on a mortgage or deed presents significant legal risks for the original poster, especially since the down payment is funded entirely by her family. His demand for joint ownership without financial contribution is unreasonable and ignores the financial risk the original poster and her father are taking. However, his feelings of insecurity are understandable as he prepares to relocate and propose, which highlights a deeper communication gap regarding their shared future.

The original poster is making the correct financial decision to keep the mortgage in her name only to protect her family’s contribution. It is recommended that they establish a formal cohabitation agreement where the boyfriend pays a fair share of household utilities and expenses, framed as living expenses rather than equity-building rent. They should also seek pre-marital counseling or financial planning together to align their long-term financial goals before proceeding with marriage.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

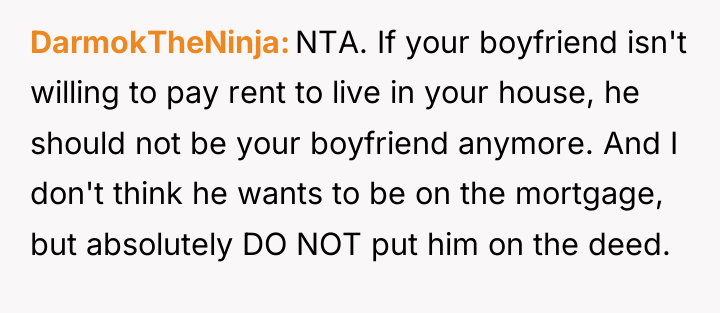

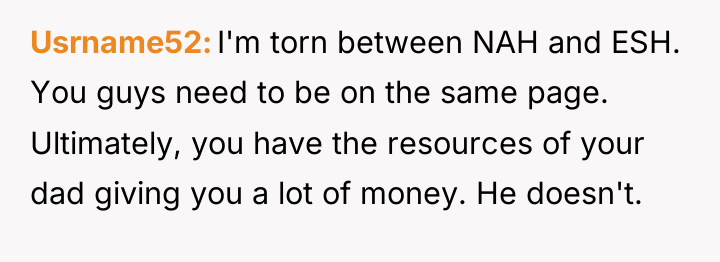

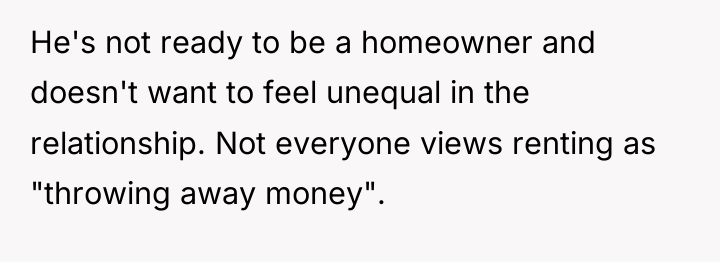

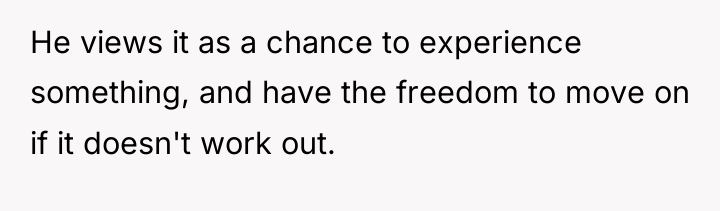

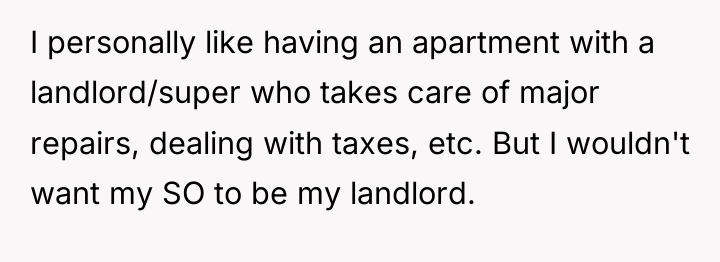

If he won’t pay and threatens you, I recommend talking to a lawyer (these are high value issues!) and finding a new BF

![[deleted] [deleted]](https://animalstrend.com/wp-content/uploads/wp-img-cache/dab68815e741901b5aa32b50799977a4.png)

The original poster is caught between her desire for financial independence and her boyfriend’s feelings of exclusion and financial anxiety. While she sees the home purchase as a secure investment aided by her father, her partner views his exclusion from the mortgage as a sign of distrust and a threat to his financial contribution to their shared future. This creates a deep rift as they try to transition into a new phase of their relationship.

Should a partner contribute financially to a home they do not own to support their relationship, or is it reasonable to protect individual assets before marriage is finalized?

{kind=link}