The user, a 26-year-old man (OP), has achieved a significant personal milestone by saving enough money to begin searching for a house. This goal has been a long-term focus for him. However, this positive development introduced a conflict immediately after he shared the news with his 23-year-old boyfriend.

The boyfriend has expressed the expectation that he should be included on the mortgage for the new home, despite having made no financial contribution to the savings or deposit. When the OP stated he was uncomfortable with this, especially given their two-year relationship length, the boyfriend reacted negatively, making repeated demands. The OP is now facing a dilemma: how to pursue his goal without upsetting his partner, who seems entitled to a share of the asset.

My Boyfriend is Upset i won’t put him on the Mortgage.

According to Dr. Logan Cooper, a specialist in financial relationship dynamics, “Financial boundaries established early in a relationship often predict the long-term stability of shared assets.” This situation highlights a classic clash between individual achievement and partnership expectations regarding resource control.

The OP is justified in protecting his asset, as a mortgage is a legal and financial commitment reflecting years of personal sacrifice, not just relationship duration. The boyfriend’s repeated demands, framed as something the OP ‘owes’ him, suggest an underdeveloped understanding of personal financial responsibility and an attempt to leverage emotional pressure to gain access to shared equity. This behavior moves beyond a simple disagreement about a house and touches upon issues of entitlement within the partnership.

The path forward requires the OP to firmly reinforce his boundary regarding the mortgage. While he should communicate his commitment to the relationship, he must clarify that major financial assets acquired solely through one party’s previous efforts should remain independent until a more formalized, long-term commitment (like marriage or a significantly longer cohabitation period with established joint financial practices) is established. Prioritizing the boyfriend’s immediate happiness over sound financial planning here could set a damaging precedent for future shared decisions.

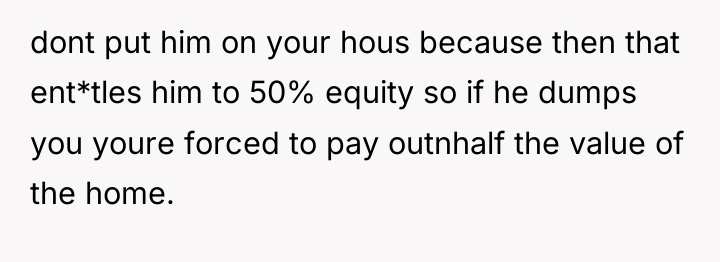

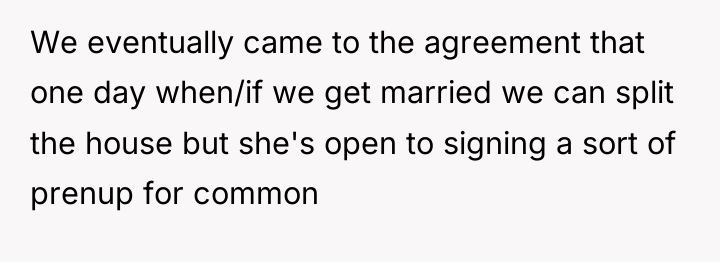

THIS STORY SHOOK THE INTERNET – AND REDDITORS DIDN’T HOLD BACK.

The central conflict for the OP is the tension between protecting a hard-earned personal asset and managing his partner’s disappointment and demanding behavior. The OP clearly views the home purchase as an individual achievement, while his boyfriend appears to view the impending purchase as a shared opportunity that entitles him to immediate co-ownership of the debt instrument.

The core question for consideration is whether the OP is being unreasonable by prioritizing his independent financial security over his boyfriend’s sense of inclusion, particularly when that inclusion involves significant financial risk for the OP. Should the OP stand firm on his decision to proceed alone, or is there an obligation to compromise on this major financial step in a two-year relationship?

{kind=link}