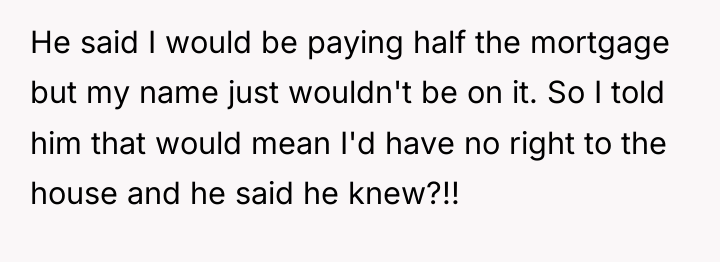

The original poster (OP), a 29-year-old woman, and her fiancé, a 30-year-old man, have been in a long-term relationship, having a child together in 2020. After OP lost her job, they moved in rent-free with her grandmother. During this time, OP focused on her education while her fiancé supported them financially and her grandmother cared for their child. The couple planned to buy a house together once OP completed her schooling.

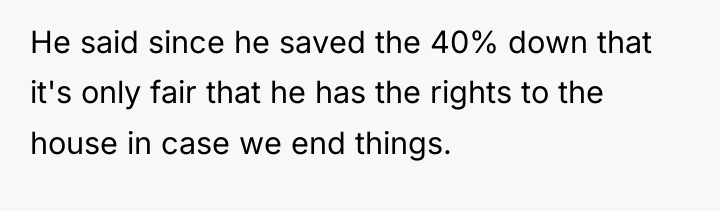

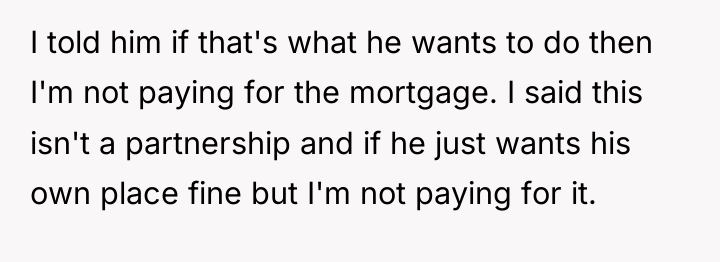

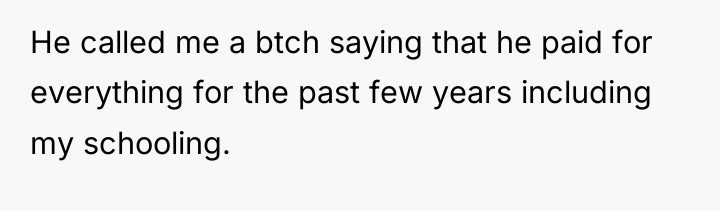

When they began seriously looking for a house, the fiancé revealed a condition: he would be the sole name on the mortgage and deed, even though OP agreed to pay half of the mortgage payments. When OP objected to having no legal ownership, he admitted this was intentional, citing his sole contribution to the 40% down payment as justification. This led to a significant conflict where OP refused to contribute financially to a property she would not own, resulting in the fiancé calling her derogatory names and demanding she uphold the initial payment agreement.

AITAH for telling my fiancé I won’t help pay the mortgage?

According to Dr. Taylor Simmons, a specialist in family finance and relationship contracts, ‘In high-value joint purchases, the principle of proportional legal ownership must align with proportional financial contribution, regardless of pre-existing savings disparities. When one party contributes labor or foregone income, that must also be factored into the equity calculation, not just the down payment.’

The fiancé’s insistence on sole ownership, while paying the down payment from his savings, reflects a desire for risk mitigation without acknowledging the concept of shared marital or partnership assets. The OP’s contribution over the past few years—providing childcare that eliminated daycare expenses, thereby indirectly supporting his ability to save and attend school—represents significant, quantifiable economic labor. By insisting the OP pay half the mortgage without granting her equity, the fiancé is essentially asking her to pay rent on a house that is entirely his, which fundamentally shifts the relationship dynamic from partners to landlord/tenant.

The OP is justified in refusing to pay the mortgage under these terms, as doing so would create an extremely vulnerable financial position for her should the relationship end. The path forward requires an immediate halt to house purchasing discussions until they can legally structure ownership (such as joint tenancy or tenancy in common) that reflects both past and future financial input, or they must accept that they are not ready to engage in major shared investments.

THE COMMENTS SECTION WENT WILD – REDDIT HAD *A LOT* TO SAY ABOUT THIS ONE.

The core conflict revolves around the OP’s expectation of a financial and legal partnership in purchasing a major asset, set against her fiancé’s unilateral decision to secure the asset solely in his name, despite her planned financial contributions and years of supporting the household in other ways. The fiancé views his financial contributions as grounds for complete ownership, while the OP views the refusal to share ownership as invalidating their partnership.

The situation forces a decision: Should the OP contribute half the mortgage payments for a house she has no legal claim to, or is she justified in withholding payment because the ownership structure contradicts the definition of a shared partnership? Readers must consider whether financial contribution without legal equity constitutes a fair arrangement in a long-term committed relationship.

{kind=link}