In the quiet moments of a shared life, love often reveals its most painful truths. After three years together, their bond felt unbreakable, a future imagined hand in hand. Yet beneath the surface of their happiness, a chasm grew—his refusal to embrace marriage clashed with her heartfelt longing for that sacred vow, leaving their dreams tangled in silent despair.

Then came a jarring glimpse into mortality, a casual joke about insurance unraveling into a raw confrontation with fear and uncertainty. Their conversation, meant to be light, exposed the fragile threads holding them together, forcing them to confront not only the possibility of loss but the profound gap in their hopes for forever.

AITA for refusing to put my BF on the title of my house or make him a beneficiary

As renowned family therapist Dr. Stan Tatkin explains, “Couples need to align on their vision of commitment—the structure, the boundaries, and the expectations of what they are creating together.” The situation highlights a significant misalignment in commitment structures between the OP and her boyfriend. The OP views marriage as the necessary legal framework that justifies merging significant assets (like life insurance beneficiaries), while the boyfriend seems to desire the emotional intimacy and partnership without the legal/financial structures of marriage.

The core issue here is a conflict over financial boundaries and the definition of commitment. The OP has maintained a clear boundary: significant financial entanglement requires the legal contract of marriage, which is a reasonable personal boundary, especially given that she owns the house solely. Her refusal is not necessarily using marriage as a ‘bargaining chip,’ but rather treating marriage as the prerequisite for the specific level of financial trust he is demanding. The boyfriend’s reaction—becoming angry and labeling her as manipulative—suggests he feels entitled to the financial benefits of marriage without agreeing to the structural commitment she requires.

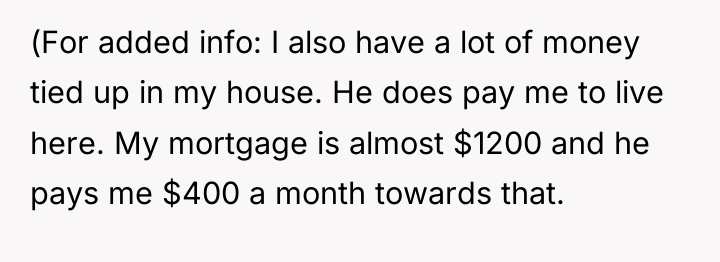

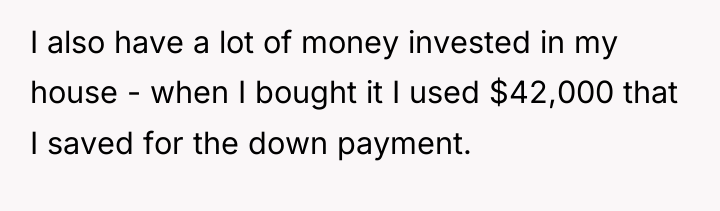

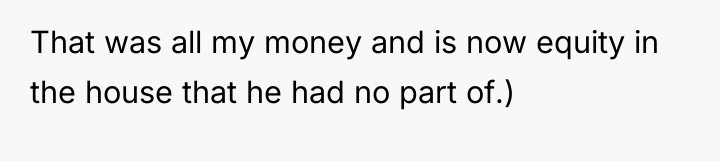

The OP’s actions in maintaining the beneficiary status were appropriate given her personal definition of commitment and the existing imbalance in asset ownership (she owns the home, he contributes minimally to the mortgage). To handle this more effectively, both parties need transparent communication that moves past vague terms like ‘not ready.’ They must explicitly define what the relationship *is* right now—a domestic partnership without marriage—and agree on what specific, non-marital financial protections (like a will or power of attorney) they are willing to put in place for each other, or accept that their fundamental definitions of commitment are incompatible.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

The original poster (OP) is facing a serious conflict where her partner, with whom she plans a long-term future, refuses to commit to marriage, which is essential to her. When the boyfriend pressured her to name him as the beneficiary on her life insurance—a financial tie usually reserved for legal spouses—the OP firmly refused based on her principle of only naming legal family as beneficiaries, linking this change only to future marriage.

Is the OP justified in maintaining strict financial separation and refusing to name her long-term, unmarried partner as a life insurance beneficiary, or is her refusal an unfair barrier that proves she is using the possibility of marriage as a manipulative tool against him, as he claims?

{kind=link}