In the fragile dance of love and boundaries, one woman dared to confront the invisible chains that bound her fiancé to his toxic family ties. With hope and courage, she voiced her pain, seeking a future where their bond could breathe freely, unshackled by the past.

Yet trust, once cracked, is a delicate thing. Despite his promises to change, the shadows of old patterns crept back silently, threatening to unravel the fragile peace they had fought so hard to build.

[UPDATE] AITA if I 29f call off my engagement to my 36m fiancé because his family have become involved in our finances

As stated by Dr. Terri Apter, an expert on modern relationships, ‘When people promise to change, but then revert to old habits, it signals that the commitment was more about immediate appeasement than true internal change.’

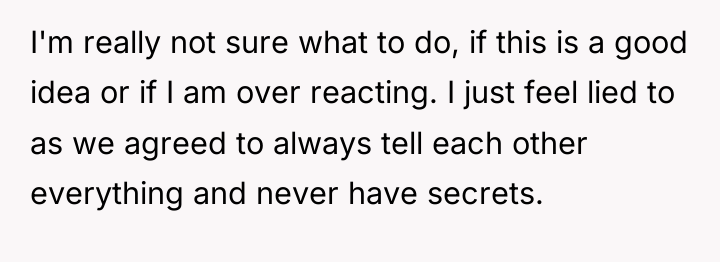

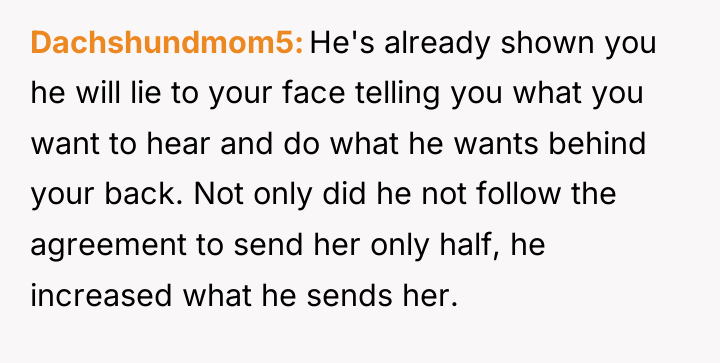

The finance partner exhibited behavior typical of ‘boundary drift’ or ‘obligation cycling.’ He initially agreed to the proposed reduction (half for six months) likely to resolve immediate conflict and avoid further confrontation, which is a common but ineffective conflict-avoidance strategy. The subsequent secret payment, exceeding even the original amount, demonstrates a failure to establish and maintain a new boundary, prioritizing his ingrained habit of financial support to his mother over his stated commitment to his partner and their shared future goals (saving for a house). The partner’s feeling of being lied to is entirely valid; the breach of trust is more significant than the monetary amount itself, especially when joint finances are involved.

The act of snooping, while ethically questionable, was driven by a pre-existing lack of security regarding the partner’s commitment, which the partner’s behavior directly caused. Moving forward with a joint bank account under these circumstances is highly inadvisable. The constructive recommendation is for the couple to pause major financial integration. They must engage in a structured discussion focusing not just on the money sent, but on *why* the partner felt the need to lie and break the agreement. Until the partner can demonstrate consistent behavioral change, maintaining separate accounts is necessary to protect the primary saver’s interests.

HERE’S HOW REDDIT BLEW UP AFTER HEARING THIS – PEOPLE COULDN’T BELIEVE IT.

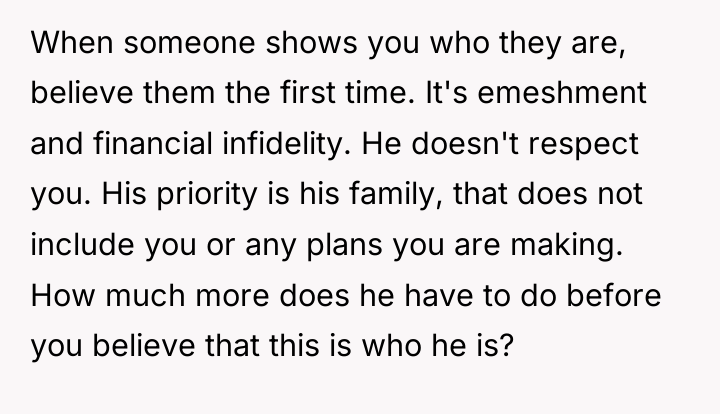

You can’t have a have a joint account with this man. And since marriage legally joins a couple’s finances, you absolutely shouldn’t marry him.

The person in this situation is experiencing deep distress due to broken trust stemming from a secret financial action by their partner, despite having reached a clear agreement about family contributions.

When a shared financial goal, like buying a house, is jeopardized by hidden behavior, is the immediate priority rebuilding faith in the partner’s honesty, or addressing the underlying pattern of boundary failure regarding financial commitments?

{kind=link}