In the shadow of unimaginable loss, she carries a secret as heavy as her grief—an inheritance cloaked in silence, a silent ledger of debts owed to the man she loved. The weight of betrayal lingers, yet she holds her peace, guarding the truth with fierce resolve, refusing to let others dictate the narrative of her sorrow.

Amidst the chaos of heartbreak, she finds strength in transformation. Leaving behind the home filled with memories that haunt her, she invests not just money but hope into a new beginning—an elegant sanctuary where healing can take root. In this new chapter, she claims her power, turning loss into legacy.

AITA for being secretive and selfish with my spouse’s life insurance benefits?

Dr. Elisabeth Kübler-Ross, renowned for her work on the stages of grief, emphasized that healing requires individuals to process loss in a way that honors their own needs, even if those needs clash with social expectations. In this scenario, the survivor is utilizing major, positive life changes—investing wisely and securing a safe, non-traumatizing home—as a proactive coping mechanism against overwhelming grief.

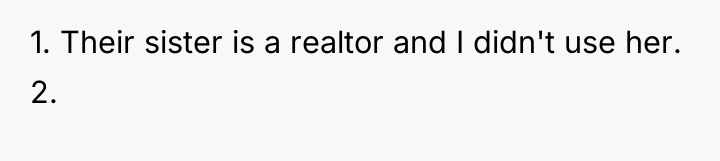

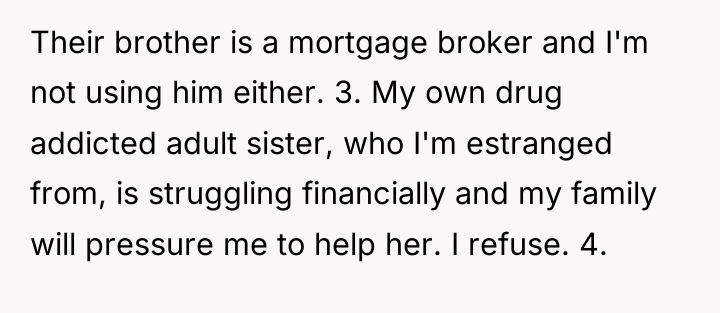

The core dynamic here involves setting and enforcing boundaries against perceived financial entitlement. The spouse’s history of lending money without the narrator’s consent, which went unaddressed, established a pattern of poor financial boundaries within the extended network. The narrator’s current actions—investing the majority of the inheritance and purchasing a home for mental well-being—are sound financial and psychological steps. The fear that disclosing the home purchase will invite judgment, requests for loans (especially from the sister-in-law realtor or brother mortgage broker), and pressure regarding the estranged sister, is entirely rational given the past context.

The decision to withhold information, while potentially leading to friction later, is currently appropriate for establishing necessary protective barriers around their emotional and financial stability during a fragile period. Constructively, the narrator should prepare a concise, non-negotiable communication script for when the move becomes apparent. This script should focus on the necessity of the move for mental health following trauma, firmly state that the inheritance is protected, and pre-emptively refuse all loan requests by citing pre-existing investment commitments, without offering details about the home’s value.

THE COMMENTS SECTION WENT WILD – REDDIT HAD *A LOT* TO SAY ABOUT THIS ONE.

Always pull the widow card too. Anytime somebody tries to give you shit about money. My HUSBAND DIED! Nothing in the WORLD can bring him BACK! What kind of sick fuck asks a WIDOW about MONEY!

Realtors and mortgage brokers both generally need to be licensed in a state to work in it. You said family lives out of state.

>He died with people owing him. They don’t know that I know. I’m not asking anyone to pay us back. As things stand, that is understandable. But don’t make not letting them know you know a hill to die on.

The individual is navigating immense grief following a traumatic loss while simultaneously managing significant sudden wealth. Their primary conflict stems from a desire for privacy and financial security versus the inevitable scrutiny and demands that large, visible assets generate from family and friends who may feel entitled to a share.

Given the clear history of financial boundary violations by in-laws and existing family obligations, is the decision to delay disclosing a major life change, like purchasing a new home, a necessary act of self-preservation, or does it risk creating deeper resentment and mistrust when the truth inevitably surfaces?

{kind=link}