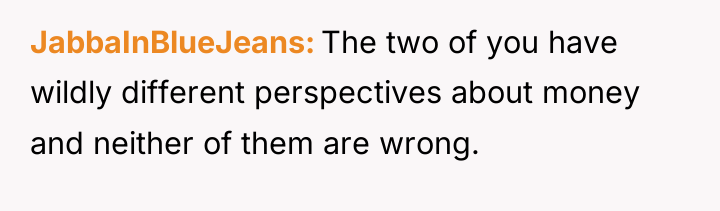

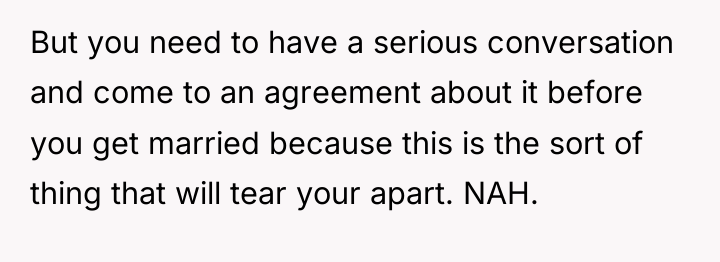

Growing up in an Asian household where family ties and collective responsibility are paramount, she was raised with the unshakable belief that finances were shared and intertwined, a sacred pact between parents and children. Her savings were not just numbers in a bank account—they were the embodiment of years of mutual support, sacrifices, and an unspoken promise to care for one another through every stage of life.

But when her fiancé, shaped by a different cultural lens and personal history, glimpsed her savings and saw only opportunity, a quiet chasm formed between them. His excitement met her firm refusal, revealing the profound clash of values beneath the surface—between individual independence and the deep-rooted tradition of family unity that defined her world.

WIBTA if I tell my fiancé he cannot use my saving for his student debt?

According to Dr. Terri Apter, an expert on family dynamics and cultural differences, ‘When partners come from different backgrounds about money, it is a major source of conflict, especially when one partner’s financial history involves intergenerational obligation.’ The core issue here is a fundamental clash in financial philosophy: the OP operates under a collectivist model where assets are shared for long-term family security, while the fiancé operates under an individualistic model typical of many Western contexts where marriage signifies a merging of individual finances for the couple’s immediate unit.

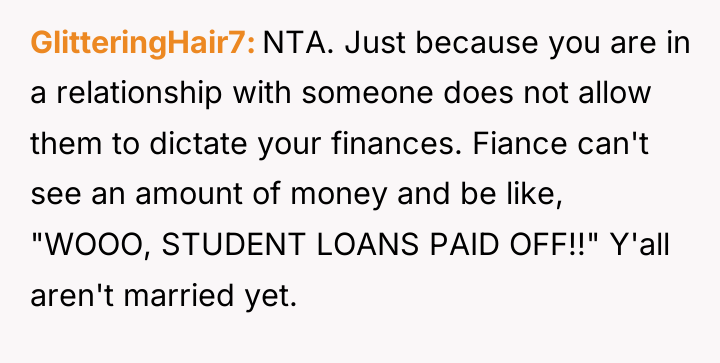

The fiancé’s immediate reaction—blowing up and accusing the OP of selfishness—indicates a failure in emotional regulation and respect for boundaries, especially given that the OP had clearly communicated the nature of these savings during dating. Demanding access to funds designated for parental support, even before marriage, crosses a significant boundary. Furthermore, the OP’s family is already providing significant economic support (free housing, covering utilities) while the fiancé is expected to contribute nothing, which weakens his moral standing in demanding access to the OP’s savings.

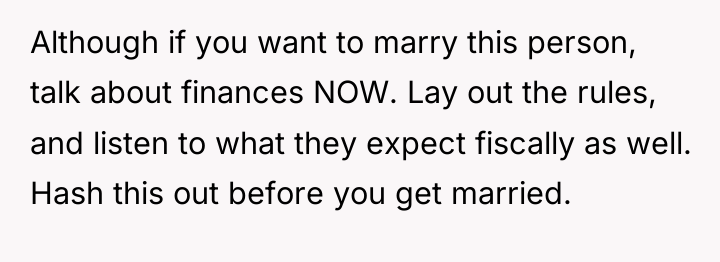

The OP’s actions in safeguarding money designated for their parents were appropriate given their cultural framework and prior agreements. A constructive recommendation for handling this situation would be for the OP to clearly articulate that these are established obligations, not personal discretionary funds. If they proceed with the marriage, future financial decisions must involve structured, documented discussions with all relevant parties—the OP, the fiancé, and the parents—to create a shared financial plan that respects both the intergenerational obligations and the needs of the new marital unit.

THIS STORY SHOOK THE INTERNET – AND REDDITORS DIDN’T HOLD BACK.

![[deleted] [deleted]](https://animalstrend.com/wp-content/uploads/wp-img-cache/dab68815e741901b5aa32b50799977a4.png)

This is raising red flags.

The individual stands firm in their belief that the savings accumulated under their cultural understanding belong to their family unit, which includes their parents. This creates a core conflict with the fiancé’s expectation that, as his future spouse in an American context, the money should be shared to resolve his personal debt.

Is it acceptable for the fiancé to feel entitled to use the partner’s dedicated family savings for his student loans without full consideration of the prior cultural understanding, or is the partner correct to prioritize the established family financial commitment over the immediate demands of their unmarried relationship?

{kind=link}