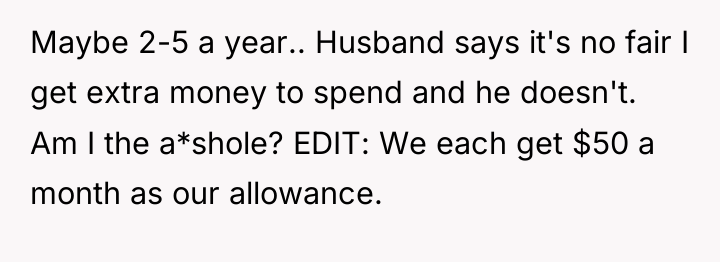

In the quiet hum of their everyday life, a subtle tension brews over something seemingly small but deeply personal—artistic passion and financial fairness. She pours her heart into occasional commissioned pieces, not for steady income but for the love of creation, while he grapples with feelings of imbalance, seeking a share of what little extra she earns. Their love is tested not by grand crises, but by the fragile threads of understanding and respect for each other’s passions and contributions.

Between the lines of shared bank accounts and monthly allowances lies a poignant struggle for autonomy and appreciation. She clings to her tiny bursts of artistic freedom, a rare spark of individuality amid the routine of motherhood and partnership. He yearns for equal footing, a fair slice of a pie that feels unevenly divided. In their story, the question is not just about money, but about honoring the small, sacred parts of themselves that keep their bond alive.

AITA because I don’t want to share my art commission money?

Dr. Terri Givens, a political scientist and relationship expert, often emphasizes the importance of financial autonomy and clear communication regarding ‘fun money’ or discretionary spending within partnerships, even when budgets are tight.

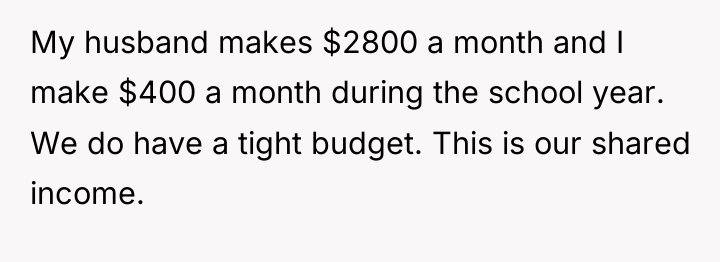

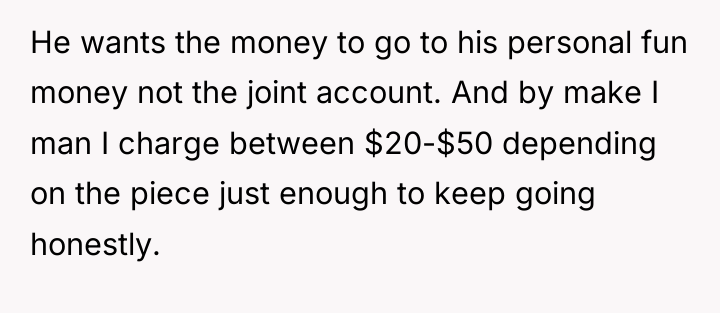

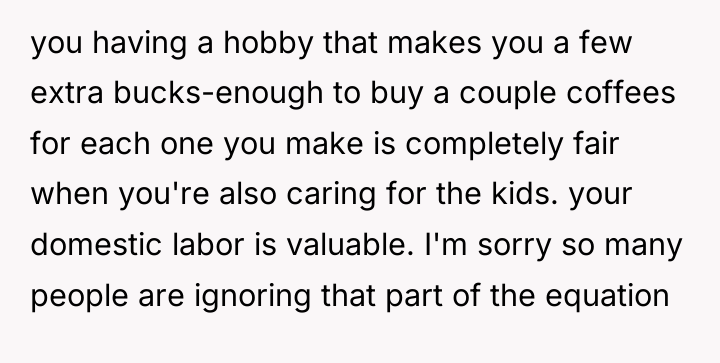

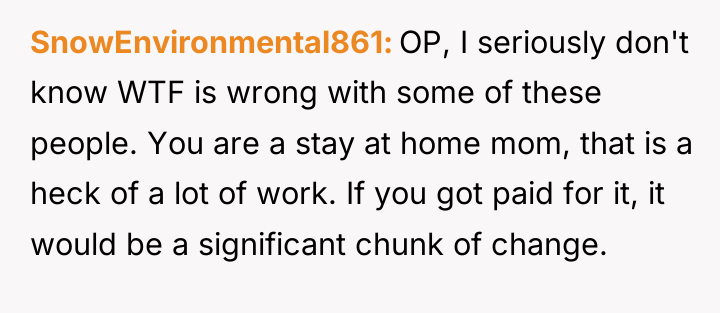

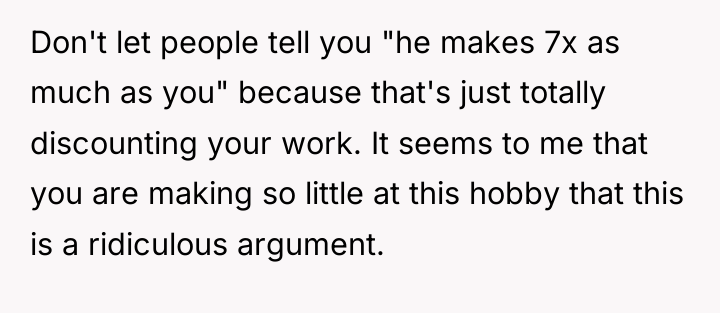

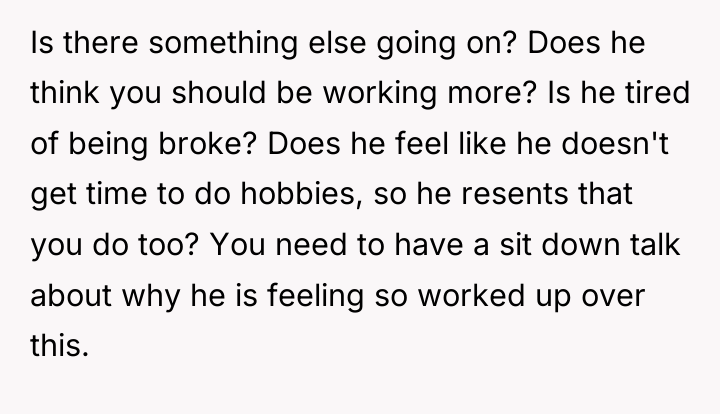

This situation highlights a common conflict in dual-income or mixed-contribution households regarding what constitutes ‘personal income’ versus ‘household income.’ The core issue is not the small sum ($20-$50 per commission, perhaps $100-$250 annually), but the principle of equitable access to discretionary funds. The husband perceives an imbalance because his allowance ($50/month) is the same as the wife’s, despite his significantly larger earned income ($2800 vs. $400 part-time). He may feel his entire contribution is strictly utilitarian, while the wife appears to have a separate, albeit small, stream of personal income funding her supplies.

The wife’s justification—using the money for hobby supplies—is a legitimate boundary, especially since the amount is inconsistent and small, resembling reimbursement for a passion rather than significant income. Her counter-offer to increase prices to create steady, substantial income for the joint account shows a willingness to contribute more formally. The suggestion that the husband might commission her art addresses the need for both his personal fun money and her hobby funding directly. For future interactions, the couple should formalize the allowance structure: if the joint account covers all shared expenses, any income below a set threshold (e.g., $100 per instance) should be deemed personal ‘hobby maintenance money,’ while anything above that threshold is contributed to the joint account to balance the perceived inequity in discretionary spending access.

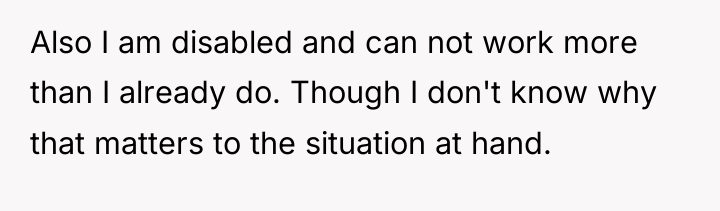

The wife’s actions in protecting this tiny income stream were understandable given the context of a tight budget and her disability limiting extra work. However, improved communication about financial needs and boundaries, rather than letting the issue remain an assumption, would be the most constructive path forward.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

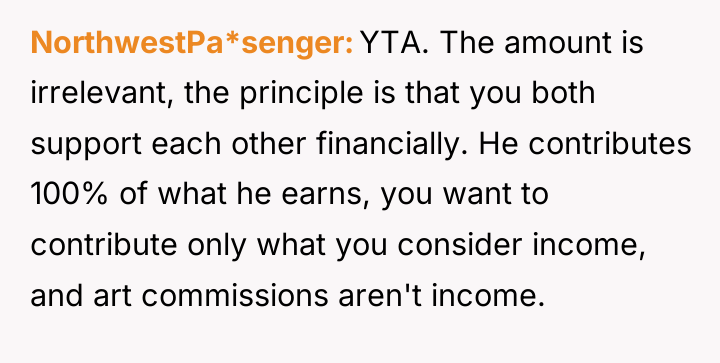

He puts everything he earns into the joint fund even though he earns much more than you do. You both get exactly the same amount of spending money out of the joint fund.

The individual in this situation feels a strong need to retain the small amounts earned from commissioned artwork, viewing it as essential for sustaining their hobby, which contrasts with their husband’s desire to merge these minor earnings into the joint funds for his personal spending money.

Given the established joint financial structure and the husband’s feeling of unfairness regarding discretionary income, is it reasonable for the stay-at-home spouse to keep the infrequent, minimal earnings from a personal creative hobby separate from shared household finances, or should all supplemental income be pooled?

{kind=link}