In the shadow of financial hardship, a family’s love and resilience forged a new path forward. After losing most of their savings in 2008, the parents faced the crushing fear of losing their home and their independence. The father, older and burdened by worry, longed to secure a future for his wife—one where she wouldn’t have to rely on their children for support.

Together, they crafted a plan born from hope and sacrifice. Purchasing a home with a large lot under their child’s name, they invested what little they had left to build a small dwelling for themselves. This arrangement promised stability, dignity, and a shared responsibility—turning a house into a symbol of family unity and unwavering commitment amidst uncertainty.

AITA for refusing to sign my parents house, which is under my name, over to my wife if I die?

As renowned researcher Dr. Brené Brown explains, “Boundaries are the distance at which I can love you and me simultaneously.” In this scenario, the OP is struggling to establish a healthy boundary between the commitment made to their parents (ensuring their housing stability) and the commitment made to their spouse (transparency and mutual financial planning). The initial arrangement involving the trust and the parents’ significant financial contribution establishes a clear, albeit unconventional, boundary regarding parental security.

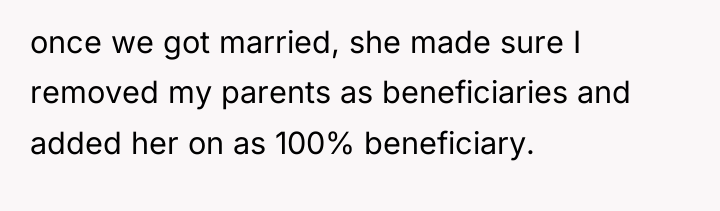

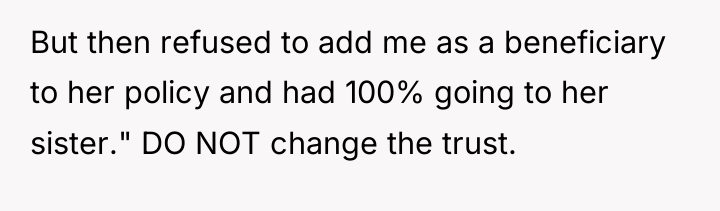

The wife’s demand to change the trust, especially following her decision to exclusively benefit her sister on her life insurance, signals a breakdown in mutual trust and equitable partnership. The OP’s discomfort is valid; giving the deed to the wife essentially bypasses the original intent of the parents’ investment and places the parents’ future housing security under the sole legal discretion of the spouse. Psychologically, the wife may be motivated by a need for financial control or fear of future uncertainty, but her approach neglects the emotional and financial contract already established with the in-laws.

The OP’s refusal to sign over the house is currently the appropriate action to maintain the integrity of the original agreement. Moving forward, the constructive recommendation is for the couple to engage in mediated financial planning that addresses both the parents’ long-term needs (perhaps by formalizing the parents’ legal right to occupy the ADU via a separate, legally binding occupancy agreement) and the wife’s concerns about shared assets, possibly through pre- or post-nuptial agreements regarding assets acquired outside this specific property arrangement.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

The original poster (OP) is experiencing significant conflict because their wife is demanding control over a property they jointly hold in trust for the OP’s parents. The OP feels a strong ethical obligation to honor the original agreement—where the parents subsidized the home’s purchase and construction specifically for their security—but this conflicts directly with the wife’s desire for property control should the OP pass away.

Considering the OP’s established commitment to their parents’ long-term housing security versus the wife’s insistence on immediate legal control, the central question remains: Is the OP justified in prioritizing the family understanding and parental welfare over their spouse’s demand to alter the property’s legal designation?

{kind=link}