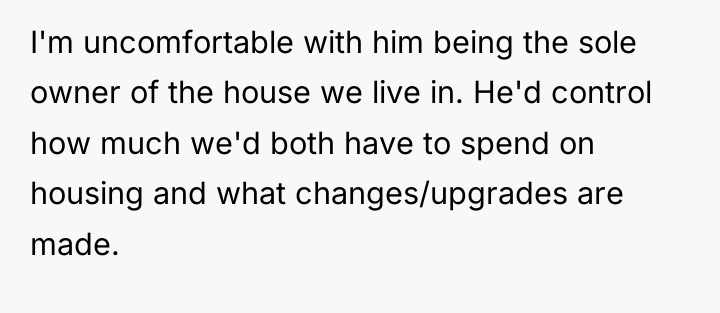

Beneath the surface of their seemingly straightforward agreement, a storm brews between two souls with clashing visions of security and sacrifice. She treasures her hard-earned savings as a shield for the future, while he wrestles with the weight of a precarious present, tethered to a house that strains his fragile finances. Their love, once a promise of shared dreams, now frays at the edges where trust and money collide.

In the quiet tension of their differing priorities, a deeper question emerges: can love thrive when financial fears overshadow hope? As he urges her to drain her savings to patch the cracks in his world, she stands at a crossroads, torn between loyalty and self-preservation, wondering if their bond is strong enough to withstand the relentless pressure of money’s invisible chains.

AITA for refusing to move into a house if I’m not a co-owner

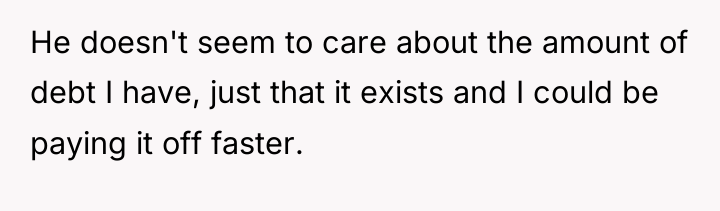

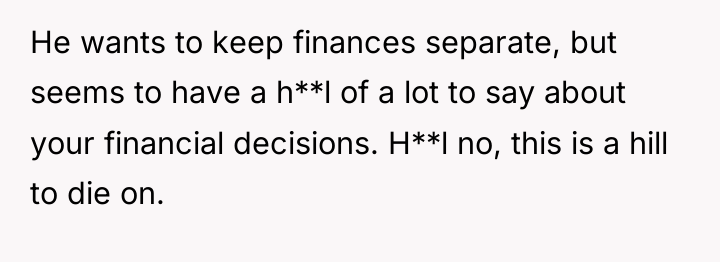

As renowned researcher Dr. Brené Brown explains, “Boundaries are the distance at which I can love you and me simultaneously.” This situation highlights a critical breakdown in establishing and respecting financial and structural boundaries within the relationship. Ben’s behavior suggests a desire to control the OP’s financial choices under the guise of ‘helping’ her pay down debt faster, effectively overriding her established financial plan which includes crucial safety nets like an emergency fund and retirement contributions.

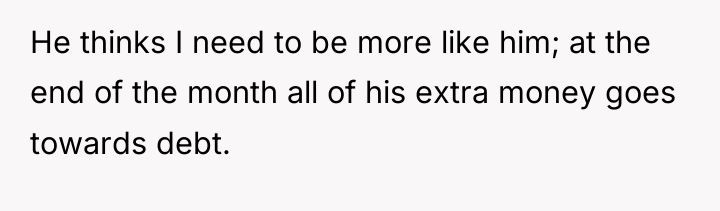

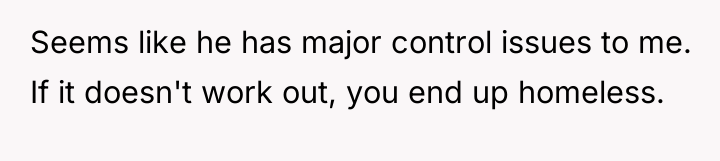

Ben’s financial approach—using high-interest debt for essential house maintenance while pressuring his partner to liquidate safe assets—demonstrates high risk tolerance and poor short-term financial management, contradicted by his criticism of the OP’s low-risk, goal-oriented strategies. The OP’s insistence on shared ownership for a primary residence is a reasonable boundary rooted in the desire for relational equality; living in a property solely owned by one partner inherently creates a power imbalance regarding housing stability and future planning, regardless of who pays the rent or mortgage share.

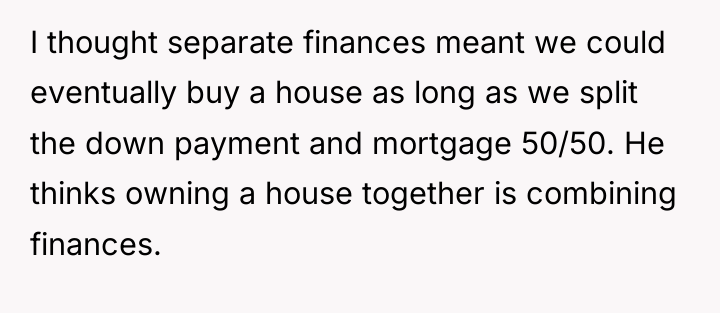

The OP’s initial agreement for separate finances likely did not anticipate a scenario where one partner would buy a large asset that the other would be expected to inhabit without any equity stake or decision-making power. The OP acted appropriately by defending her established financial safeguards and refusing to move into a situation where her housing security and autonomy are compromised. Moving forward, the couple must clearly redefine what ‘separate finances’ means in the context of shared major assets like a home, perhaps seeking premarital counseling to align on long-term visions rather than adhering to rigid, unworkable interpretations of past agreements.

THIS STORY SHOOK THE INTERNET – AND REDDITORS DIDN’T HOLD BACK.

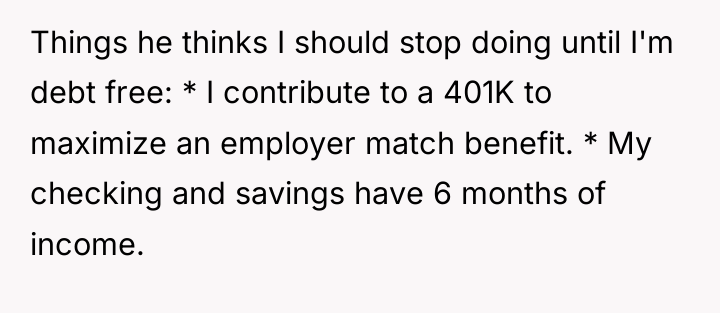

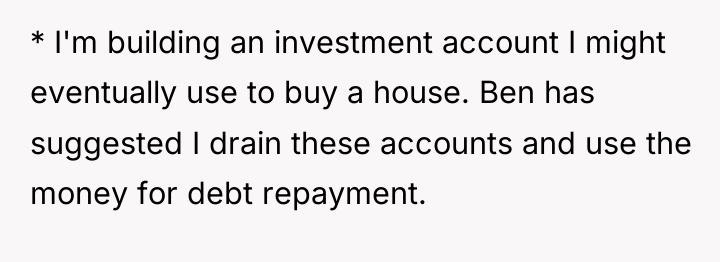

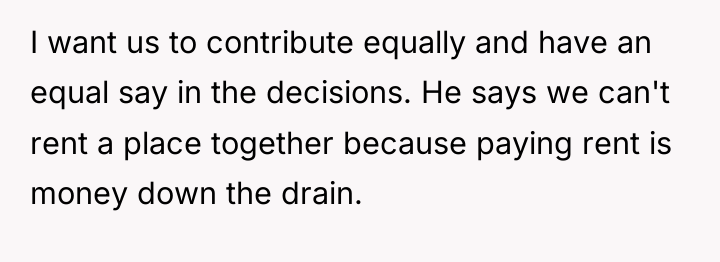

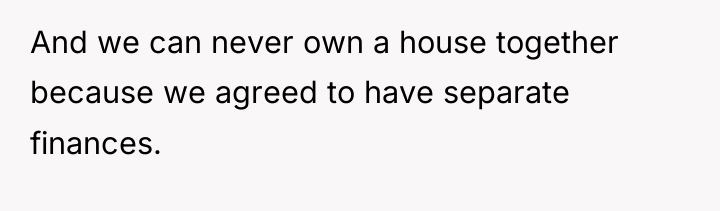

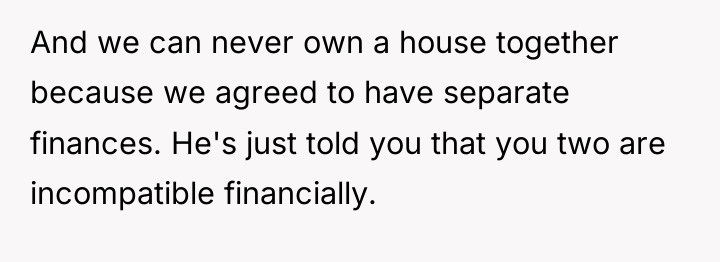

The original poster (OP) is in a conflict where her financial priorities, focused on saving and long-term security (401k match, emergency fund, investments), clash directly with her partner Ben’s insistence that she aggressively pay down her subsidized student loans immediately. Furthermore, the disagreement has escalated around shared living arrangements, as OP values shared ownership and equal decision-making in a future home, while Ben insists she move into his sole-owned, expensive property or remain separate, viewing shared homeownership as combining finances against their initial agreement.

Given that the OP is financially responsible by conventional metrics but holds different priorities than Ben, is the OP justified in refusing to move into a property she does not co-own when Ben equates shared housing with combining finances, thereby undermining her need for equal say in major housing decisions?

{kind=link}