In the delicate dance of merging lives and dreams, a newlywed couple stands on the threshold of their first shared home. She carries the weight of years spent saving every penny, a testament to resilience and hope, while he brings the comfort of family support and a different kind of security. Their journey is more than just a financial transaction—it’s a profound testament to their love, sacrifice, and the blending of two very different pasts into one future.

Yet beneath the surface of their joint venture lies a quiet tension, a clash of values and expectations shaped by their unique histories. As they prepare to lay down roots, the true cost of their dream reveals itself—not just in dollars, but in the emotional currency of trust, compromise, and the unspoken stories that define who they are and what they’re willing to give for the life they want to build together.

AITAH for telling my husband he needs to pay me back for the down payment discrepancy for our house purchase

Dr. Gail Dines, a sociologist who has studied contemporary family finance, often notes that financial merging is one of the most significant stressors for newly married couples, especially when there are pre-existing disparities in saving habits or asset accumulation.

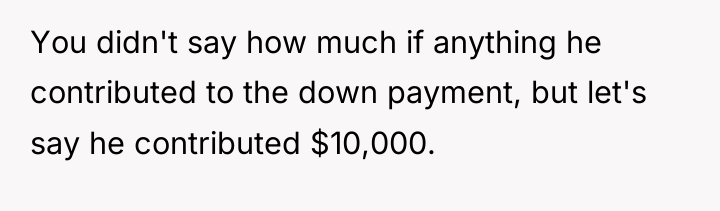

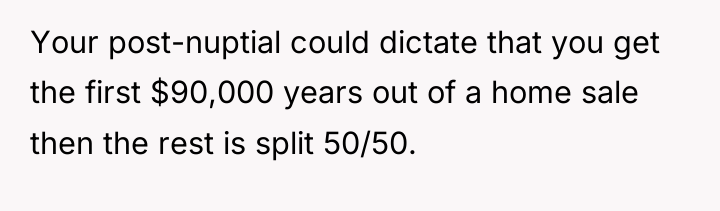

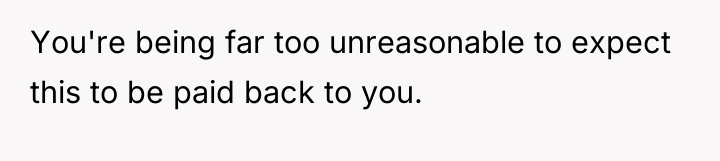

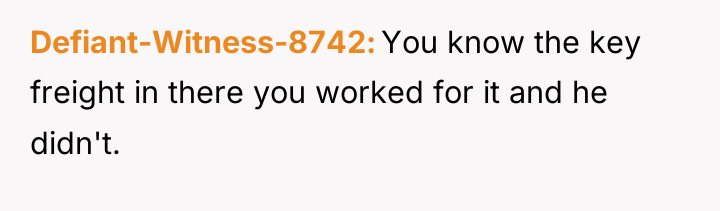

The situation presented highlights a critical misalignment in financial philosophy. The poster views her $80,000 down payment as an individual asset earned through deferred gratification, leading to a reasonable expectation of equitable contribution toward the new home’s equity structure. Her husband, conversely, operates under the ‘complete merging’ model common in traditional marital vows, where ‘his money is mine and vice-versa.’ This difference is amplified because the husband benefited from lower living expenses historically, leading to a larger perceived budget without the same personal sacrifice the poster endured to build her savings. The husband’s reaction to the request for a repayment plan suggests an avoidance of acknowledging the disparity in effort and contribution.

The OP’s request to be paid back over time is a practical attempt to establish equitable reimbursement for the cash injection that benefited the shared marital goal (the house). While the husband’s ‘we are married’ stance is common, it fails to respect the financial realities established *before* this specific joint purchase. The OP’s action was appropriate in raising the equity issue. For future effectiveness, instead of demanding ‘repayment’ (which sounds like a loan between two people), the couple should use a financial planner to document the exact percentage of equity each person brings to the closing table. This creates a transparent paper trail reflecting actual contributions, satisfying the OP’s need for fairness while respecting the legal reality of joint ownership.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

The poster is deeply conflicted, feeling that her significant financial contribution, earned through years of hard work and sacrifice, is being dismissed by her husband under the premise of marital unity. Her core conflict lies between her strong belief in individual financial responsibility and her husband’s expectation that all assets immediately become joint property upon marriage.

Should the couple prioritize maintaining clear financial accountability for individual contributions to a shared asset, or does the commitment of marriage inherently supersede personal savings distinctions, requiring all funds to be pooled without expectation of repayment?

![[Update] AITAH for breaking up with and kicking my girlfriend out because she went to an afterparty without me?](https://animalstrend.com/wp-content/uploads/2025/10/featured-39130-1760536385-350x250.jpg)

{kind=link}