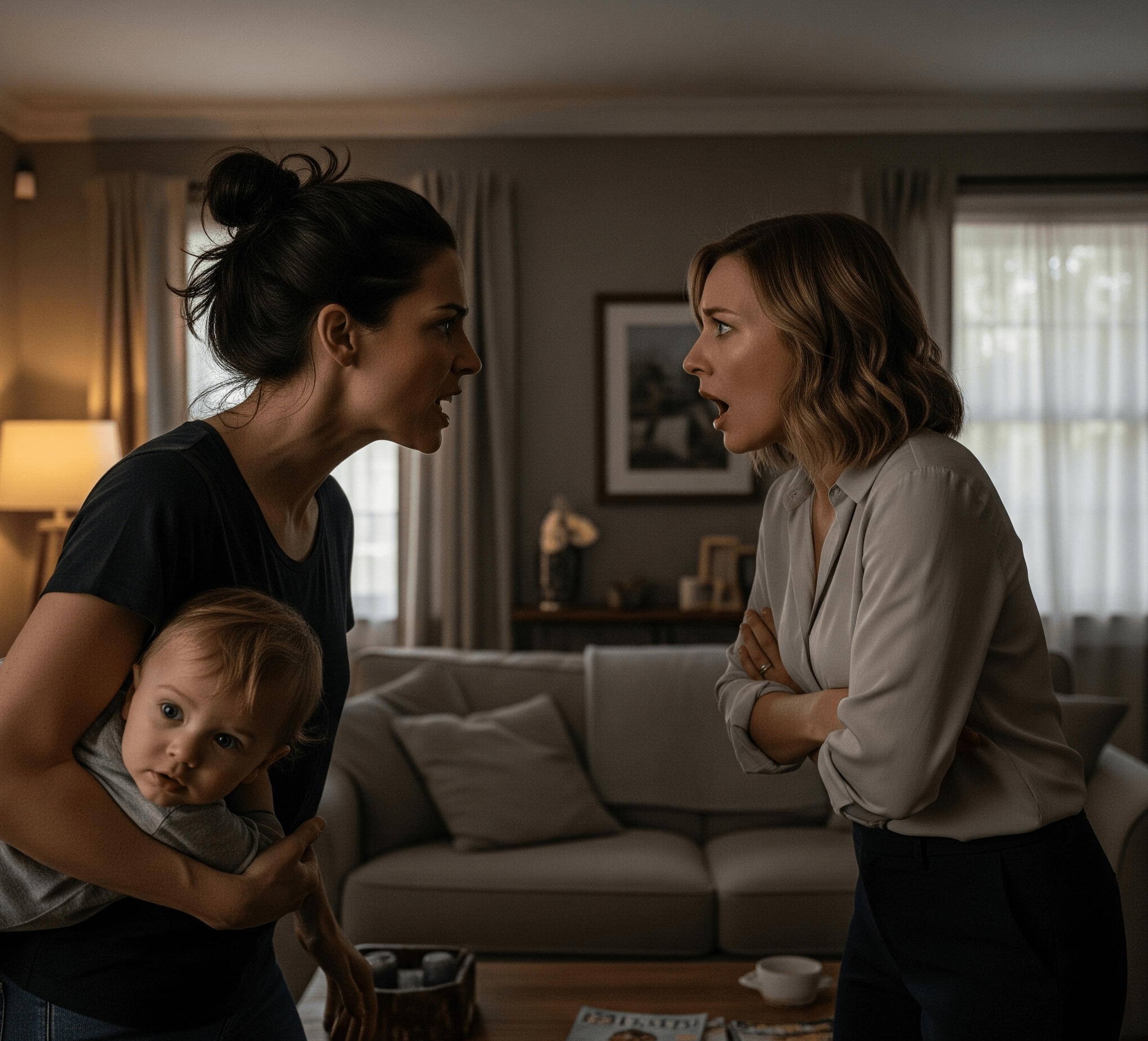

Caught between familial duty and looming risk, a young woman faces an overwhelming decision. At just 21, she’s asked to co-sign a $200,000 mortgage for her brother and father—strangers to her daily life, separated by distance and circumstance. The promise of no financial burden feels fragile against the harsh reality that her name alone could anchor a heavy debt she never intended to bear.

Her heart wrestles with love and caution as she uncovers the truth behind the co-signing agreement. The weight of responsibility clashes with her desire to support her family, revealing the fragile line between trust and vulnerability. In this silent battle, she confronts the fear of losing control over her future, all while trying to protect those she holds dear.

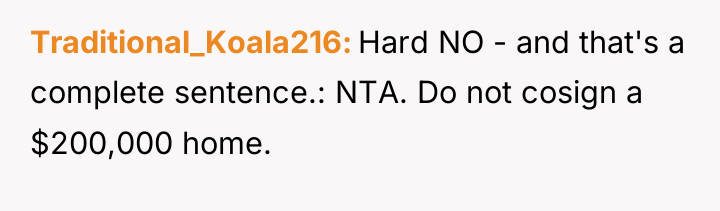

AITAH for not cosigning a mortgage agreement for my parents?

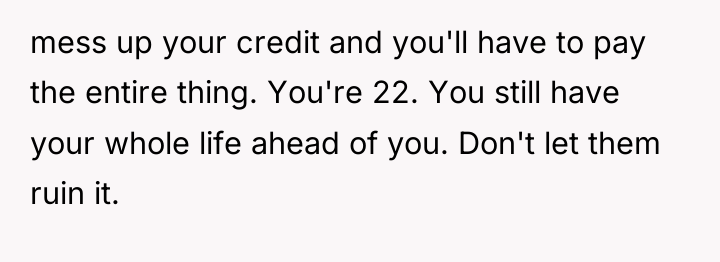

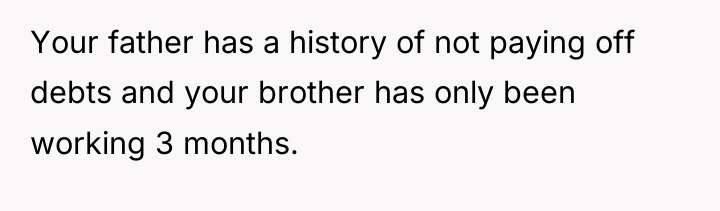

According to financial literacy experts like Suze Orman, co-signing a loan means taking on 100% of the legal responsibility for the debt if the primary borrower defaults. This is not merely an act of goodwill; it is a legal and financial entanglement that can severely damage the co-signer’s credit score and expose their assets to seizure. In this scenario, the OP is being asked to place her financial future, potentially impacting her military career stability or future housing prospects, on the line for a $200,000 obligation where one borrower has a history of bankruptcy and the other has minimal employment history.

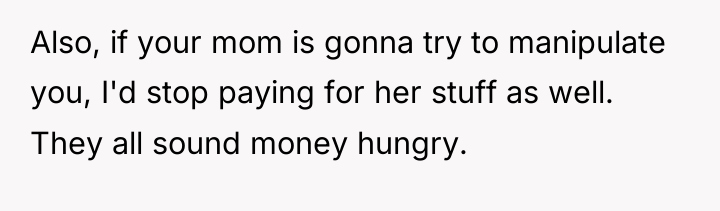

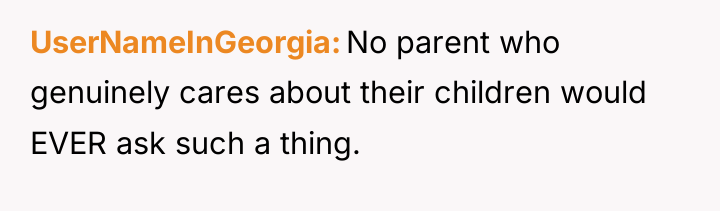

The mother’s reaction—equating the OP’s prudent financial caution with a personal failing or a lack of love for the father—is a classic example of emotional manipulation, often termed ‘guilt-tripping.’ This tactic shifts the focus from the legitimate financial risk assessment to the OP’s perceived moral character. Furthermore, the mother minimized the OP’s existing financial contributions (paying for insurance and phone bills) while framing this mortgage cosignature as the ‘only’ help required, demonstrating a disregard for the scale of the liability being requested.

The OP’s actions in researching the commitment and expressing hesitation were entirely appropriate and responsible. Constructively, in the future, when faced with similar high-stakes requests, the OP should maintain clear boundaries, stating that her financial decisions are based on verifiable data, not emotional appeals. A constructive alternative would be to offer a smaller, non-liability-based form of support, such as helping them research first-time homebuyer programs or improving credit scores, rather than accepting open-ended legal risk.

HERE’S HOW REDDIT BLEW UP AFTER HEARING THIS – PEOPLE COULDN’T BELIEVE IT.

The original poster (OP) faced immense pressure from her family to cosign a significant mortgage based on trust and perceived familial duty, despite legitimate financial risks stemming from her father’s past bankruptcy and her brother’s short employment history. Her hesitation, rooted in rational financial self-protection, led to an emotional backlash from her mother, who framed her caution as a lack of love and support for her father.

Is it justifiable for family members to leverage emotional obligation and guilt to compel a relative to assume severe, uncompensated financial liability based on promises that overlook documented risk factors, or should personal financial security always take precedence over familial requests for high-stakes guarantees?

{kind=link}