For fifteen years, she has lived in the shadow of her husband’s financial control, a silent struggle masked by their comfortable life. Despite his substantial income, her access to money is tightly restricted, leaving her to navigate motherhood and household responsibilities with limited freedom and constant negotiation over every dollar.

Now, faced with a sudden inheritance—money meant to be hers—she stands at a crossroads, yearning for independence and respect within her marriage. The desire to safeguard her financial autonomy clashes with the fear of conflict, as she contemplates whether she can claim a separate space for herself in a world where control has long been dictated by another.

AITA for wanting to keep my inheritance?

According to family finance expert and author of ‘The Total Money Makeover,’ Dave Ramsey, financial intimacy requires transparency and shared goals, but it does not negate the need for personal financial boundaries, especially when dealing with inheritances which are often viewed as separate property.

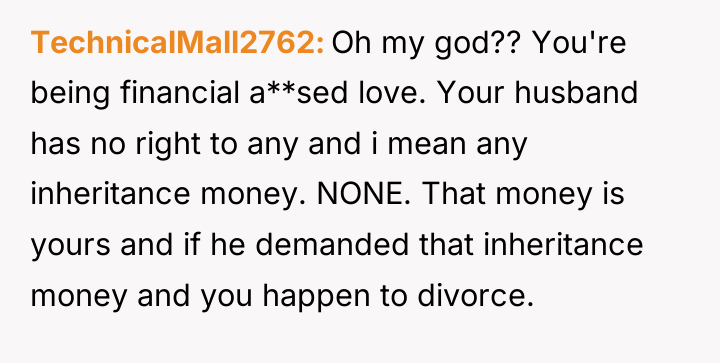

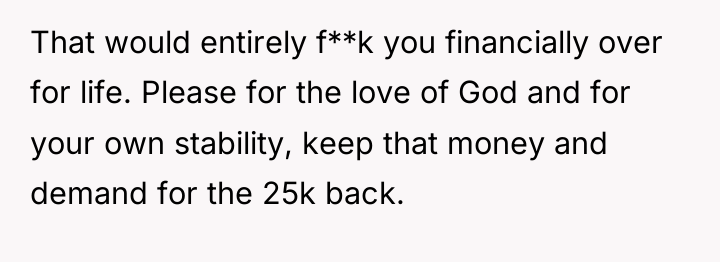

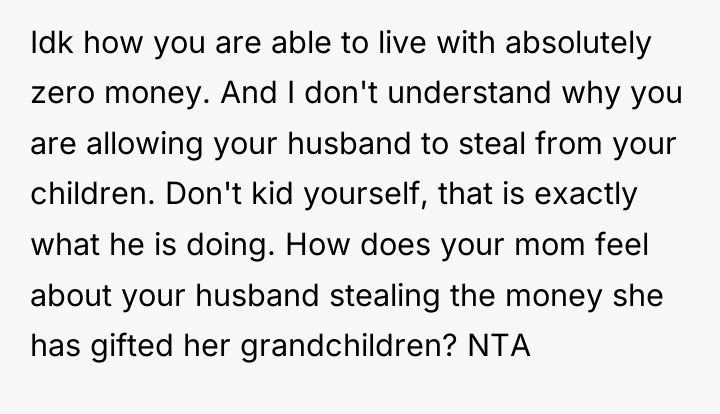

The core issue here is not merely investment strategy but a long-standing pattern of financial control, which creates a significant power imbalance in the marriage. The husband’s behavior—taking previous gifts and restricting the wife to minimal discretionary funds ($1k annually or $500/month based on his proposed investment)—suggests a lack of trust and an intent to maintain total financial authority. The wife’s fear that she will ‘never see a dime’ and will be ‘stuck financially’ upon his early retirement is a rational response to this dynamic. Her desire to place the $50,000 in a separate savings account in her name is a necessary step toward establishing financial safety and boundary setting.

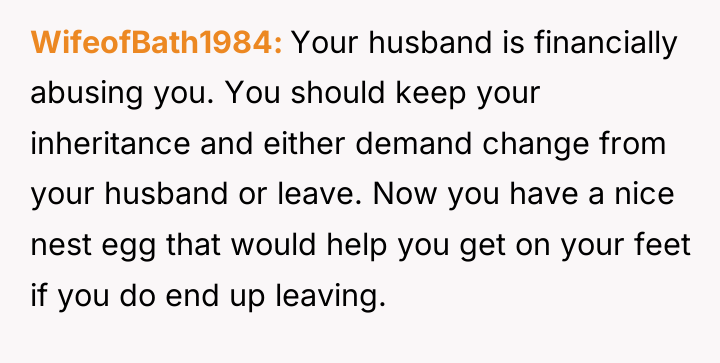

The expectation that she must hand over an inheritance to him, especially when he plans to use the resulting income as her ‘allowance’ while simultaneously planning for his early retirement and her subsequent employment, indicates a lack of equitable planning for their shared future. The wife’s actions should prioritize establishing access to liquid funds under her sole control. A constructive future step involves seeking pre-marital or financial counseling to address the controlling behavior directly, framing the request not as distrust, but as a requirement for personal security in the event of unforeseen circumstances.

THIS STORY SHOOK THE INTERNET – AND REDDITORS DIDN’T HOLD BACK.

The wife finds herself in a position of severe financial dependence, where her husband controls access to money, even from her own inheritance. Her desire for a small degree of financial autonomy clashes directly with her husband’s established pattern of controlling all household investments and major assets.

Given the established history of financial control, should the wife assert her right to keep her $50,000 inheritance separate for her own security, or is she obligated by the structure of their 15-year marriage to hand the funds over to her husband for joint investment?

{kind=link}