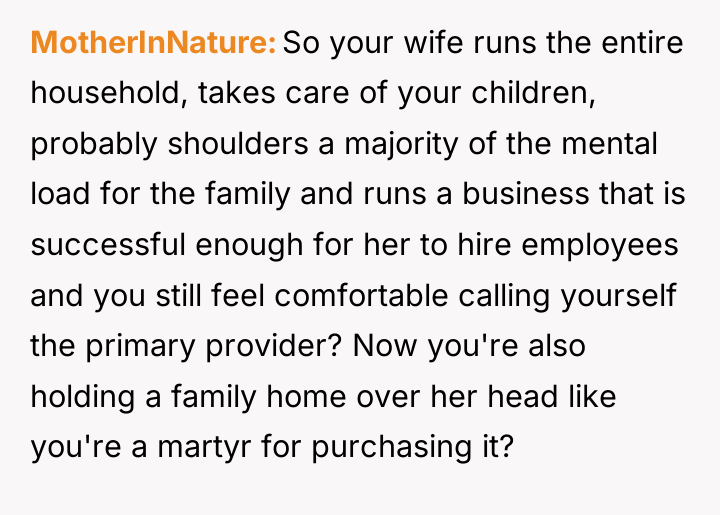

In the quiet tension of their upscale new home, a man wrestles with the unspoken costs of love and ambition. His wife’s dreams of entrepreneurship fill the basement with endless inventory, turning their shared space into a battleground of priorities and sacrifice. Though he foots the lion’s share of their financial burden, the weight of unacknowledged contributions strains the very foundation of their marriage.

Caught between provider and partner, he insists his mortgage payments are more than just dollars—they are his way of supporting her dreams. Yet, this claim ignites a deeper conflict about value, recognition, and the invisible labor that underpins their fragile harmony. In their struggle to balance love, business, and home, the true cost of success reveals itself in the silent cracks of their relationship.

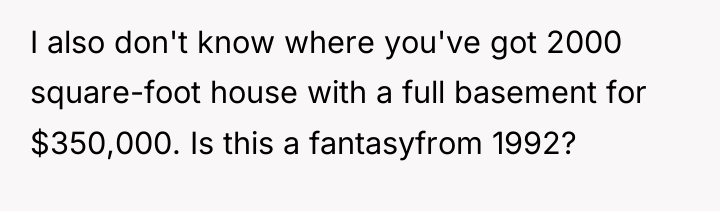

AITA for insisting that my sole provider payment of a $350,000 mortgage counts as a business expense for my wife’s home business?

Dr. Terri Givens, an expert in family finance and communication, often emphasizes that financial contributions must be viewed within the context of agreed-upon household roles and shared goals. In this case, the structure of contributions is heavily skewed, placing the husband in the role of sole provider for a luxury asset (the large home) that directly benefits one partner’s business.

The husband’s motivation stems from feeling unappreciated and overburdened; he perceives paying 90% of the income and the entire mortgage for a house twice the size of what he deems necessary as a massive contribution to the business’s infrastructure. The wife’s refusal to categorize the large house as a luxury, and her insistence that the mortgage payment does not equate to ‘helping organize,’ demonstrates a failure to acknowledge the financial foundation supporting her venture. This situation highlights a significant boundary issue: the husband feels his financial sacrifice should exempt him from physical/organizational labor related to the business, while the wife is demanding a direct monetary contribution toward the operational upkeep (the organizer’s fee).

The husband is not the asshole for feeling his mortgage contribution is substantial, but his framing of it as the sole contribution to organization is flawed. A better approach would involve a direct, non-emotional negotiation about the division of labor versus financial contribution for the business space. The professional recommendation is for the couple to formally quantify the basement space—e.g., 75% for the business requires 75% of the associated organizational cost. If the husband covers the housing luxury, the wife should cover the full cost of organizing her inventory, or they must agree on a percentage split for the organizer’s fee based on space utilization.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

She’s not a business woman, she’s running an MLM from the garage on your dime

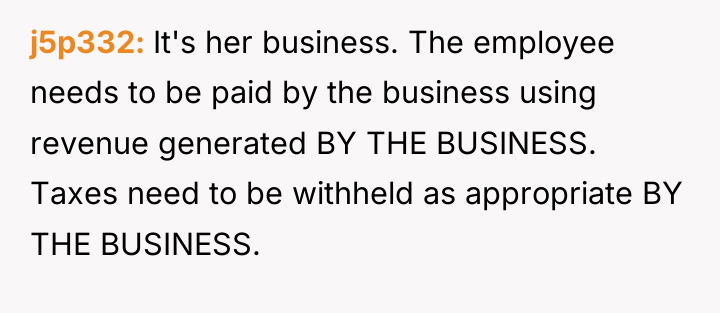

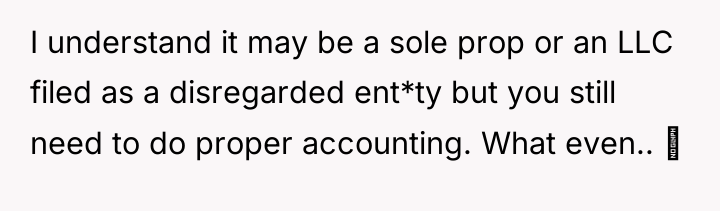

The fact that you admitted she had such a bad spending issue that you had to separate finances and she won’t tell you how much she makes now or contribute to the household finances is a major issue as well

The husband feels his overwhelming financial contribution, especially covering the large mortgage for the new house that facilitates his wife’s business, should negate his responsibility for organizing the resulting inventory clutter. The central conflict arises because the wife views his mortgage payments as simply covering basic housing necessities, not as a specific contribution to her business operations, leading her to demand he pay for supplementary organizational help.

Given that the large house is a shared asset enabling the wife’s growing enterprise, is the husband’s complete funding of the $2,500 monthly mortgage sufficient contribution to the business’s organizational needs, or is paying for external organizing help a separate, necessary cost the primary earner should bear?

{kind=link}