In the wake of a profound loss, a family grapples with the tangled emotions and unexpected revelations left behind. The discovery that a recently deceased father named his child as a beneficiary ignites a quiet storm of confusion, loyalty, and unspoken tensions between a mother and her children.

Caught between honor and heartache, the child wrestles with the weight of an inheritance that feels both like a gift and a burden. Amidst the grief, the boundaries of entitlement and fairness blur, leaving a fragile family to navigate the delicate balance of love, loss, and legacy.

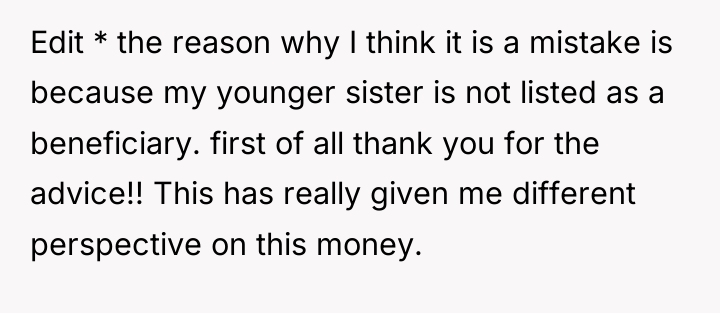

Mom wants me to sign over 250k beneficiary check

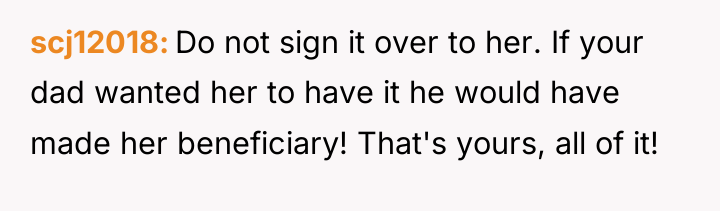

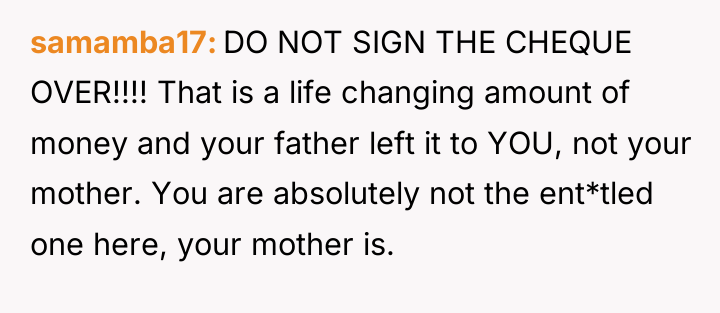

As noted by financial and estate planning experts like those cited by the American Bar Association, legally named beneficiaries on life insurance policies typically override informal family wishes, as these policies are generally considered non-probate assets intended to pass directly to the named recipient. The policy designation reflects the deceased’s most recent, legally binding intent regarding that specific asset.

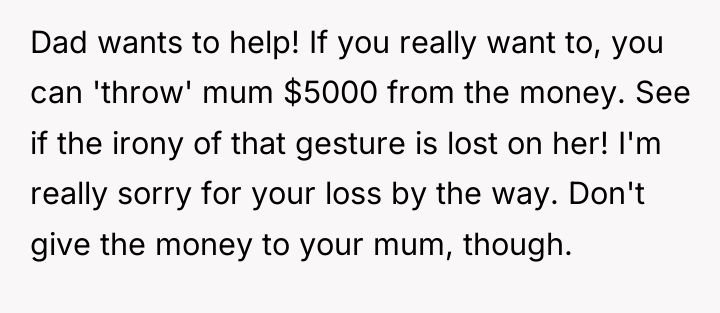

The situation presents a classic conflict between legal entitlement and emotional obligation, often heightened during periods of grief. The initial stance of the original poster (OP) to give the money to the mother reflects a strong desire to maintain relational harmony, likely driven by the psychological need to support the surviving parent and preserve a good relationship. However, the mother’s subsequent offer of only $5,000—a small fraction of the total sum, especially when the OP is financially strained—suggests a potential power imbalance or an underestimation of the OP’s own financial needs and the significance of the inheritance.

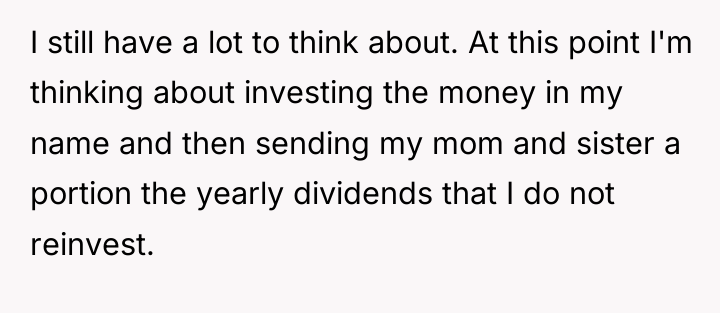

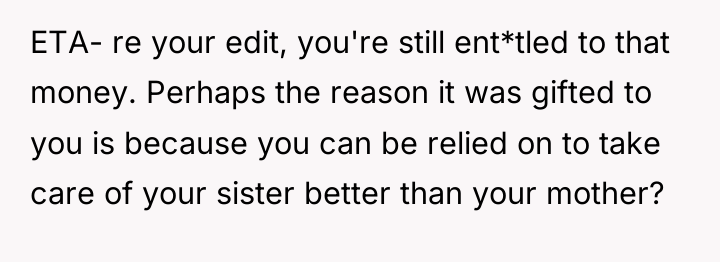

The OP’s revised plan to invest the money and distribute dividends seems like a balanced, albeit complex, compromise aimed at honoring the inheritance while providing ongoing support to the mother and sister. A more direct approach might involve clearly communicating personal financial needs first, then proposing a specific division that honors the mother’s loss while acknowledging the OP’s own financial standing. The key is shifting the focus from ‘handing over’ the money to ‘jointly planning’ how these unexpected funds can best support all surviving family members without sacrificing the OP’s own financial security.

AFTER THIS STORY DROPPED, REDDIT WENT INTO MELTDOWN MODE – CHECK OUT WHAT PEOPLE SAID.

![[deleted] There are no mistakes when making a life insurance...](https://animalstrend.com/wp-content/uploads/wp-img-cache/8d5dc49c8d4553d0efc8fbea80e5e70f.png)

![[deleted] Oh dear lord... don't do it! Your mum is...](https://animalstrend.com/wp-content/uploads/wp-img-cache/27011ec8591132c87f1a37144c280c5e.png)

The individual is navigating a difficult situation following a parent’s death, caught between honoring a legal document and meeting a parent’s strong request regarding life insurance funds. The core conflict lies in the tension between the legal designation of the money and the mother’s expressed desire for control over the distribution, complicated by the offer of a small portion of the funds for a significant life event like a wedding.

Given the unexpected inheritance and the mother’s significant existing assets, is the mother’s demand for the full transfer of the beneficiary funds justified by familial expectation, or does the named beneficiary have a right to the funds based on the deceased’s final wishes? Where should the line be drawn between filial duty and individual financial autonomy in this sensitive post-loss scenario?

{kind=link}