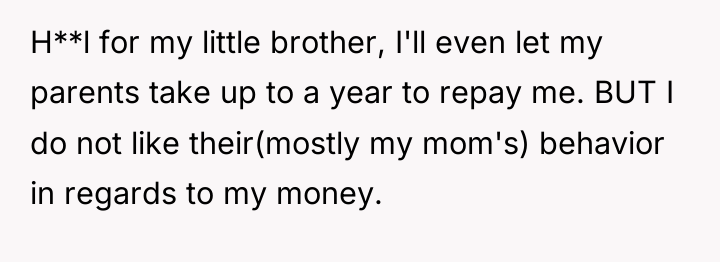

At just 20 years old, he carries the weight of his family’s financial struggles on his young shoulders. With $7,500 saved up—$2,300 in cash—he stands as both a lifeline and a reluctant lender to parents who, despite their net worth, live trapped by looming mortgages and diminished incomes. His heart breaks for his little brother, who desperately needs braces, and he’s willing to shoulder the cost, even if it means bending over backward for a family that can’t seem to respect the boundaries of money and pride.

Yet beneath the surface of generosity simmers a quiet frustration. His parents’ uneasy attitude toward repayment, especially his mother’s awkward behavior around his finances, strains the fragile balance between love and money. He wants to help without feeling taken advantage of, but the line keeps blurring, leaving him caught in a painful dance of support, resentment, and hope.

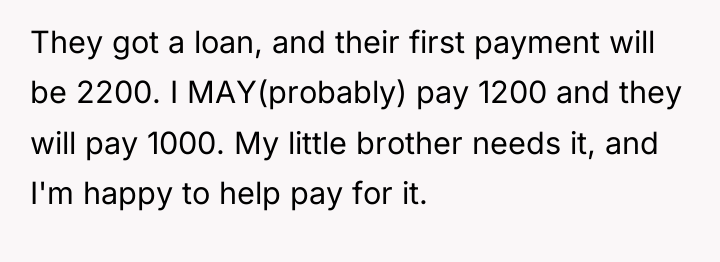

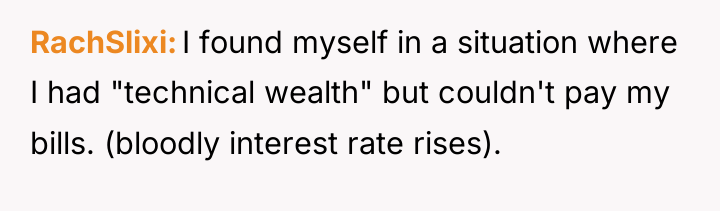

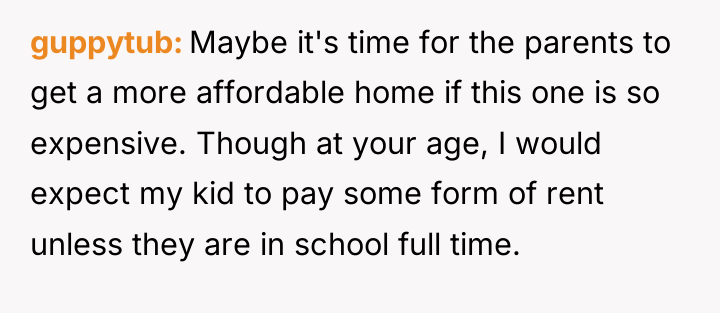

AITA for asking my mom to hurry up with deciding if she needs my $1200 or not?

According to Dr. Harriet Lerner, a noted psychologist specializing in family dynamics, ‘Boundaries are not about controlling other people; they are about deciding what is acceptable for you.’ In this situation, the conflict centers on a breakdown of clear financial boundaries, despite the parent-child relationship.

The core issue is transactional ambiguity layered over an emotional relationship. The parents are leveraging their role as providers (free housing/food) to dismiss the son’s legitimate request for financial accountability regarding a personal loan. When the son asks for a timeline, he is seeking predictability and respect for his financial autonomy—a standard adult expectation. The mother’s response (‘Why are you so selfish, all you care about is money’) is a classic deflection technique, shifting the focus from the financial agreement to an attack on the son’s character. This creates immense emotional pressure, forcing the son to choose between his financial security and perceived familial love.

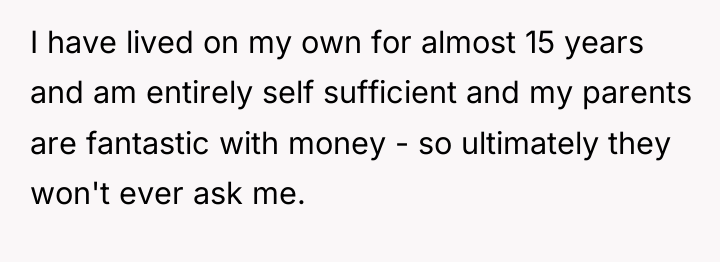

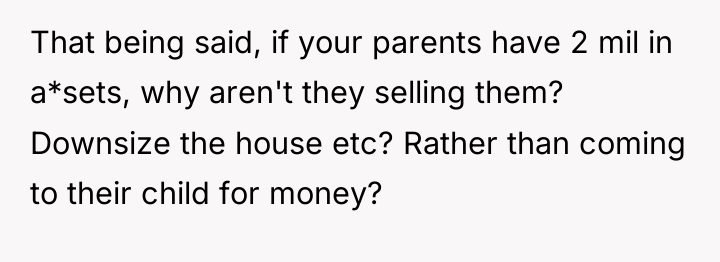

While the parents are financially wealthy overall (implied by the $2-3 million net worth), their current cash flow stress is real, making the loan necessary. However, treating a zero-interest loan like an unlimited demand is inappropriate, especially when the lender (the son) is also young and saving. The son’s request for a repayment timeline is completely reasonable and not selfish. A constructive recommendation is for the son to frame future discussions around ‘agreements’ rather than ‘loans,’ perhaps agreeing to defer repayment contingent on the parents meeting specific financial milestones or providing a firm, written commitment for a date range, removing the emotional component from the necessary transaction.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

![[deleted] [removed]](https://animalstrend.com/wp-content/uploads/wp-img-cache/3f7bc766abd9de9412cf72f408e04477.png)

![[deleted] The first thing is unless your brother's dental situation...](https://animalstrend.com/wp-content/uploads/wp-img-cache/32566fb51c28a37796c240f97c51b0a3.png)

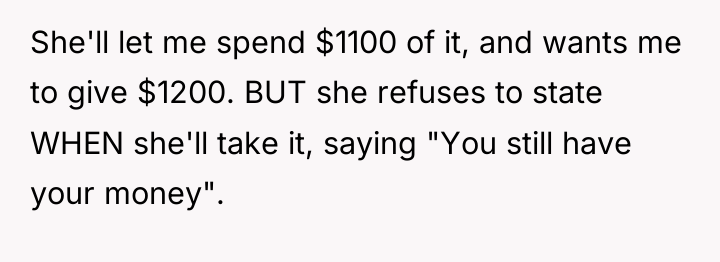

The 20-year-old individual is facing a difficult emotional conflict. They genuinely want to support their family, particularly their younger brother’s dental needs, but they feel disrespected and anxious about their parents’ casual and unpredictable handling of the money they have loaned.

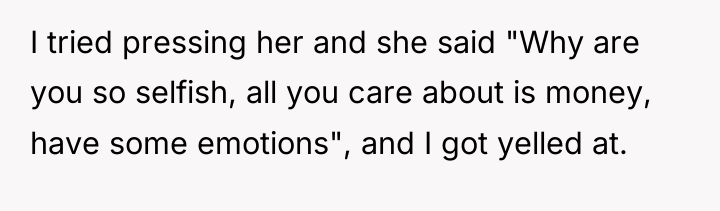

Is the young adult wrong for demanding a clear repayment schedule for a personal loan, or is the parents’ reaction—labeling the request as selfish—a valid defense given they provide free housing and food?

{kind=link}