In the quiet tension of their home, two souls grapple with the fragile balance of trust and financial survival. She, a newcomer to this land, fights to build a life and a credit history from scratch, while he carries the weight of past mistakes that threaten to pull them under. Their love is tested not by lack of care but by the silent fears that money can sow between hearts.

Caught between the desire to protect her hard-earned progress and the hope of unity he insists upon, she wrestles with the boundaries of marriage and independence. Their arguments over plastic cards and credit scores are more than just numbers—they are battles for security, respect, and the future they both desperately want to share but fear to risk.

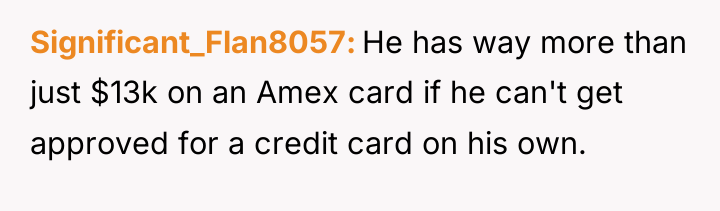

AITA for not letting my husband with $13k debt have access to my credit card

As noted by financial therapist Dr. Brad Klontz, a leading expert on money psychology, ‘Financial infidelity and mismatched financial values are among the top predictors of marital dissatisfaction and divorce.’ This situation highlights a classic conflict where differing financial histories and values clash immediately following a merger of lives.

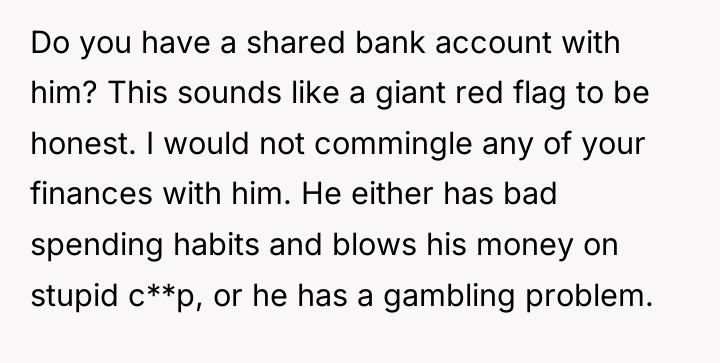

The husband’s argument that married couples must share assets aligns with a traditional view of marital unity, but it fails to account for the unique context: the wife is actively rebuilding her financial foundation in a new country. Allowing an authorized user status to someone with existing significant debt ($13k) and a history of mismanagement introduces extreme liability. The wife’s concern is not about sharing; it is about liability, as an authorized user’s activity directly impacts the primary account holder’s score.

The wife’s hesitation is rooted in legitimate risk management, especially given her recent immigration status and lack of established credit infrastructure. The feeling of guilt, stemming from the husband’s past support, is an emotional complication that should not override sound financial planning. A constructive path forward involves decoupling emotional debt from transactional credit decisions. The narrator was correct to protect their credit. The future recommendation should focus on financial education for the husband (as mentioned in the update) and the establishment of clear, separate financial boundaries, perhaps starting with joint financial planning sessions rather than immediate shared liability accounts.

HERE’S HOW REDDIT BLEW UP AFTER HEARING THIS – PEOPLE COULDN’T BELIEVE IT.

![[deleted] [removed]](https://animalstrend.com/wp-content/uploads/wp-img-cache/3f7bc766abd9de9412cf72f408e04477.png)

The narrator feels conflicted, torn between the desire to support their spouse and the urgent need to protect their fragile, newly established credit history. The central tension exists between the societal expectation that married couples share financial lives and the narrator’s personal, practical reality of starting credit from zero.

Given the significant financial risk to the narrator’s future, is prioritizing the establishment of individual credit a justifiable defense of self-interest, or does this action violate the expected unity and trust inherent in a marriage?

{kind=link}