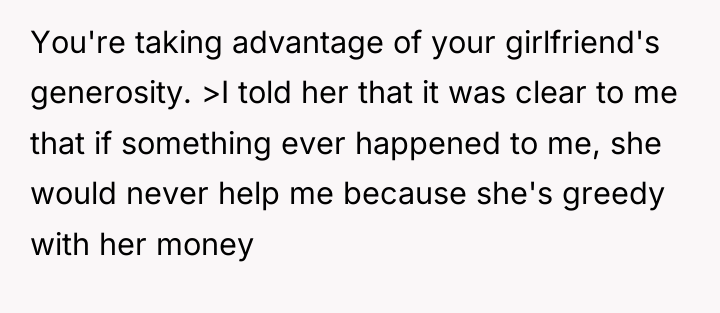

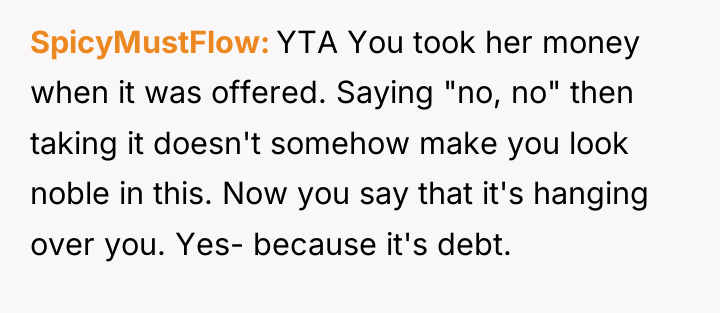

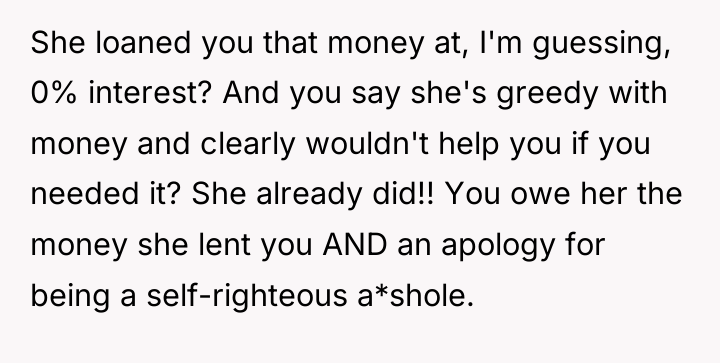

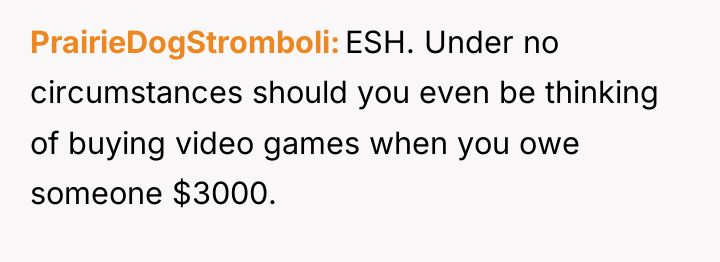

He once saw a glimmer of hope when she offered to help with a $3,000 personal loan, a lifeline during his darkest financial struggles. But what began as kindness soon turned into a heavy chain, binding him with pressure and guilt, making every dollar spent on himself feel like a betrayal.

Despite his efforts to stay afloat, paying her back faster than the bank demanded, every attempt to enjoy his simple pleasures is met with reminders of debt and obligation. What was meant to be a favor now feels like a relentless weight, eroding his freedom and peace of mind.

AITA for telling my girlfriend I’m only going to give her a bit of the money I owe her after winning the lottery

Psychologist Dr. Ramani Durvasula notes that when personal loans replace formal agreements, they often become tools for control rather than simple transactions, stating, ‘When money moves between close relationships, it rarely stays just about the money; it becomes about power, obligation, and emotional leverage.’

The dynamic described illustrates a significant issue of boundary erosion and emotional labor. The lender initially offered the loan with flexible terms (‘pay her back in my own time’), but immediately undermined this flexibility by exerting control over the borrower’s non-debt-related spending (the gaming hobby). This suggests the lender views the debt as justification for continuous oversight of the borrower’s finances, violating the initial agreement. Furthermore, the borrower, despite being in debt, is financially supporting the relationship by paying for food and driving, creating a power imbalance where the lender is both the creditor and a financial dependent in day-to-day expenses, yet leverages the debt for moral authority.

The borrower’s decision to prioritize savings was appropriate from a sound financial management perspective, as having an emergency fund mitigates future reliance on others, especially given the lender’s demonstrated lack of reliability in managing the debt situation fairly. However, the manner in which the $1,500 was allocated—telling the lender the plan after the fact—provoked the conflict. A more constructive approach would have been to communicate clearly before the lottery win, reinforcing the boundary that responsible repayment includes building a financial safety net, especially since the lender has shown they would not assist in an emergency.

THIS STORY SHOOK THE INTERNET – AND REDDITORS DIDN’T HOLD BACK.

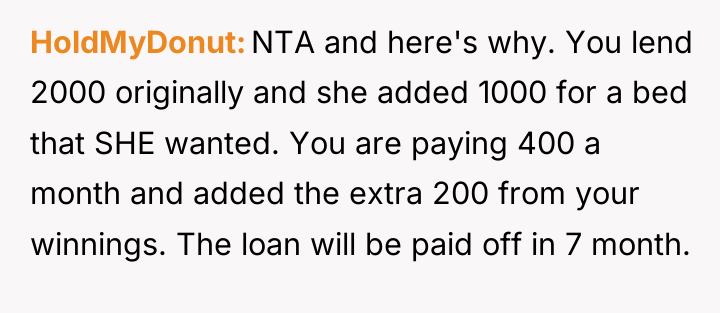

![[deleted] [deleted]](https://animalstrend.com/wp-content/uploads/wp-img-cache/dab68815e741901b5aa32b50799977a4.png)

A) repaying your debt to her

B) building an emergency fund

The “emergency fund” is another selfish excuse _disguised_ as an attempt to be financially mature, when it’s the opposite. Pay her back.

You’re joking, right?

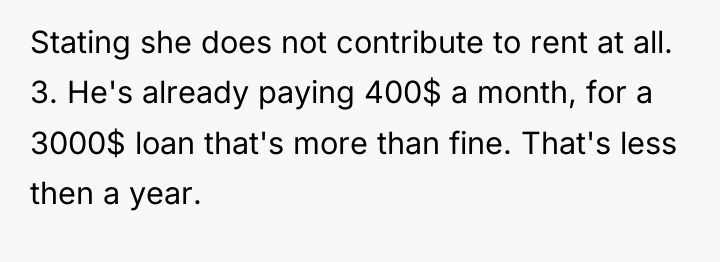

![[deleted] NTA. The sub of double standards is at it...](https://animalstrend.com/wp-content/uploads/wp-img-cache/1549cf2e7955fbbbca6d2616fcd78349.png)

The individual experienced significant stress and resentment after receiving a personal loan, as the informal agreement led to continuous financial pressure and unsolicited judgment from the lender regarding personal spending. The conflict intensified when the lender became angry over the individual’s decision to allocate lottery winnings toward building an emergency fund rather than solely accelerating debt repayment.

Given the breakdown in trust and the current strained living situation, the central question remains: Was the decision to prioritize a small contribution to an emergency fund over immediately satisfying the lender’s demands a justifiable act of self-preservation, or did it represent a breach of the implied good faith required when accepting significant personal financial assistance?

{kind=link}