A retired man, having carved out a comfortable life through fortunate investments, finds himself at a crossroads of generosity and family loyalty. When his nephew struggles to balance the pressures of a demanding job, wedding plans, and a home purchase, the man steps in with an interest-free loan, a gift born from belief in the young couple’s future and a desire to ease their burden.

Yet, the gift that was meant to unite and support instead stirs tension beneath the surface. While his nephew and brother express heartfelt gratitude, the sister-in-law’s call reveals a simmering conflict, hinting at the fragile dynamics that money can ignite within even the closest of families.

AITA For Giving My Nephew A 50k Loan As A Wedding Gift?

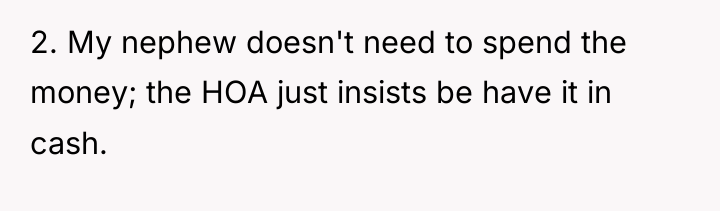

1.

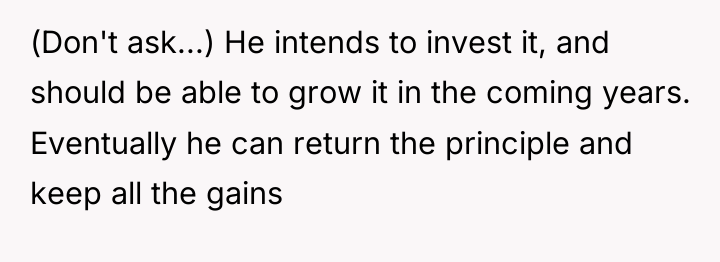

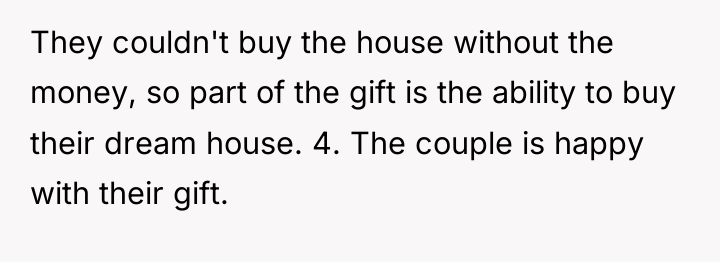

3.

According to Dr. Harriet Lerner, a clinical psychologist known for her work on boundaries and family dynamics, ‘When we act in ways that protect our own sense of rightness or generosity, while ignoring the feelings or expectations of others, we often create predictable conflict.’ In this situation, the 55-year-old narrator acted based on his perception of generosity—an interest-free loan intended to solve an immediate financial hurdle for his nephew.

The core issue here revolves around differing interpretations of financial support and boundary management. The narrator views the $50,000 as a gift because of the zero interest and the potential for the nephew to benefit from the investment timeline. However, the sister-in-law (SIL) defines a gift by its permanence; money that must be repaid, regardless of favorable terms, remains a debt, not a finalized transfer of wealth. The SIL’s reaction suggests she perceives the loan as an insufficient contribution compared to the scale of the wedding/house purchase, or perhaps she feels slighted by being excluded from the decision-making regarding the primary financial gift. The narrator’s response of buying registry items after being labeled ‘miserly’ indicates a reactive move to preserve family peace rather than a genuine desire to fulfill the registry, which can be detrimental to setting future financial boundaries.

The narrator’s initial action was extremely generous from a purely financial standpoint, directly solving a $35,000 closing cost problem. The complexity arises from the relational aspect. For future interactions, the narrator should establish clear terms—even for ‘gifts’ that are structured as loans—to manage expectations proactively. If the intent is purely a gift, the funds should be gifted outright. If the intent is a loan, it should be documented as such, regardless of the interest rate, to align expectations with reality. A better approach would have been to state clearly, ‘This is a $50,000 loan to help with closing costs, due back when you are financially stable, with no interest,’ thereby owning the transaction as a loan from the start, which might have preempted the SIL’s objection.

THE COMMENTS SECTION WENT WILD – REDDIT HAD *A LOT* TO SAY ABOUT THIS ONE.

![[deleted] NTA](https://animalstrend.com/wp-content/uploads/wp-img-cache/14b5c3e09c6d5f006ebcb372d59bb968.png)

I’d take an interest free 50k loan over a silverware set as a wedding gift in a heartbeat.

I think you’re being incredibly generous. You aren’t giving them a “physical” gift, sure. But you’re gifting them a head start on their future.

Your loan *was* a gift. Even though you expect the principal balance back eventually, you gifted them open-ended deadline with no interest and, as you said, *the ability to buy their home*.

The narrator experienced internal conflict after offering substantial financial aid to his nephew as an interest-free loan, believing it to be a generous gift that enabled a major life goal. This act, intended as helpful and unconditional support, was harshly redefined by the sister-in-law as cheapness because the principal was expected to be returned.

Is the nature of a large, interest-free loan, offered without a fixed repayment schedule, truly a gift when the recipient is obligated to return the principal sum, or does the sister-in-law’s expectation for an additional, tangible registry purchase invalidate the significant financial accommodation already provided?

{kind=link}