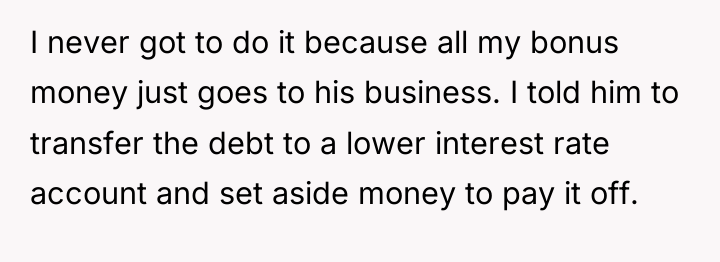

She carries the weight of the world on her shoulders—juggling a demanding job, graduate studies, household duties, and the emotional toll of constantly bailing out her struggling husband. Despite being the family’s backbone and provider, she feels invisible, overwhelmed, and exhausted, her own needs buried beneath endless responsibilities and stress.

Amid the chaos, her husband’s sudden purchase of a new car sparks a fragile hope that things might be turning around. But beneath the surface, the cracks widen—resentment, unspoken fears, and financial strain collide, unraveling their fragile balance and threatening to shatter the life they’ve been desperately trying to hold together.

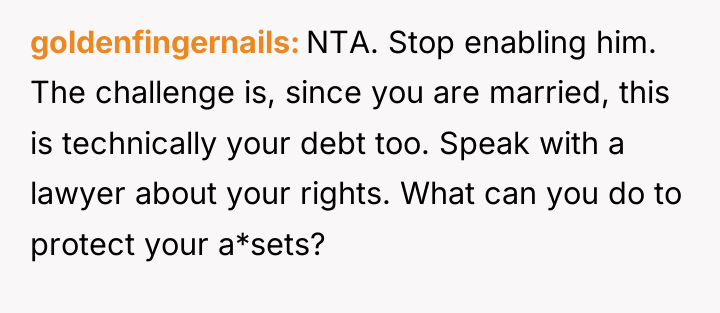

AITA if I don’t pay off my husband’s debt

According to relationship expert Dr. John Gottman, healthy relationships require both partners to feel supported and valued, often emphasizing ‘turning toward’ bids for connection. In this scenario, the wife is clearly depleted, unable to meet her husband’s needs for intimacy or attention because her resources (time, energy, and money) are continually redirected to subsidize her husband’s failing venture. The husband’s complaint about quality time, while perhaps a genuine bid for connection, occurs immediately after he made a major purchase (a new car) despite his undisclosed financial distress, suggesting a severe breakdown in financial transparency and partnership accountability.

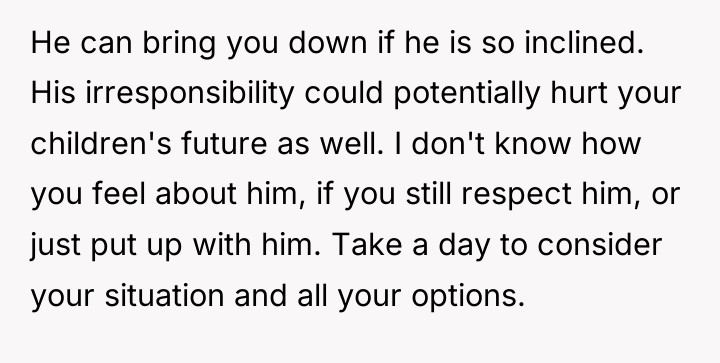

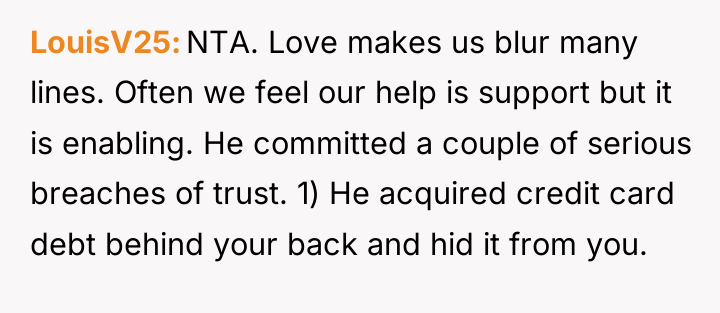

The power dynamic here is heavily skewed. As the primary breadwinner who also manages the majority of domestic labor and now studies, the wife is performing significant ’emotional labor’ and ‘financial labor’ without adequate reciprocity. The husband’s behavior—hiding business struggles, accruing $10k in credit card debt, and complaining about intimacy—indicates a failure to maintain personal responsibility. When a partner repeatedly uses another’s income to cover chronic business shortfalls, it erodes trust and autonomy. The wife’s realization that her bonus money is perpetually funding a cycle of failure rather than shared goals (like home improvements) is a critical turning point.

The wife’s decision not to bail him out this time appears appropriate, provided she has clearly communicated the boundary and offered a structured alternative, which she seems to have done by suggesting debt consolidation and a structured repayment plan. For future effectiveness, she should formally decouple her income from his business liabilities. A constructive recommendation is to establish strict financial boundaries where business losses are treated as his sole responsibility moving forward, while her income is clearly allocated first to shared household expenses and savings goals, treating her bonus as her discretionary fund for previously agreed-upon needs.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

![[deleted] I think you should cut him off at the...](https://animalstrend.com/wp-content/uploads/wp-img-cache/a94012cd3b422413637e4bc3c9d7de5c.png)

![[deleted] NTA. Seems he doesn't have much of a business....](https://animalstrend.com/wp-content/uploads/wp-img-cache/b699c179cecc803616d7d89d02b1ac53.png)

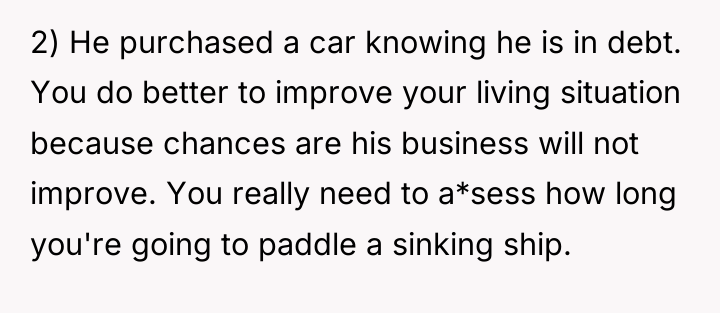

But why is he permitted to continue with his hobby. If it’s not breaking even, it’s not a business or a job.

The wife finds herself in a deeply stressful situation, balancing being the sole provider, managing the home and children, and pursuing graduate studies. Her conflict centers on the repeated financial rescues of her husband’s failing business versus her own long-deferred personal and household needs. She is emotionally exhausted from carrying the entire financial and domestic load.

Given the history of repeated financial bailouts that have not resulted in long-term stability for the husband’s business, is the wife justified in refusing to pay off his current $10,000 credit card debt this time, choosing instead to allocate her substantial bonus funds toward necessary home improvements she has postponed for years?

{kind=link}