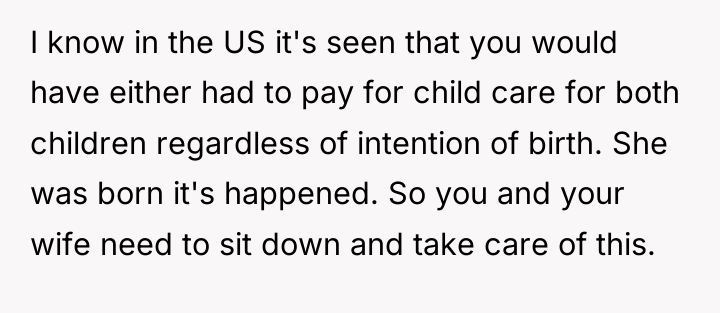

Eighteen years ago, a promise was made in the quiet hope of balancing dreams and responsibilities. A family, once small and simple, pledged to grow with clear terms — one child fully supported by the wife, who insisted she would bear every cost of their second child’s life and passions. It was a delicate bargain born from love, yet shadowed by underlying tension, as the husband’s cautious heart feared the weight of unspoken debts.

But time has a way of shifting tides and revealing truths hidden beneath years of assumed trust. The wife, once a stay-at-home mother, stepped into a new role with a rising salary, quietly changing the financial landscape they once agreed upon. What began as a shared journey now teeters on the edge of unspoken questions and unmet expectations, where love battles with the reality of promises left unfulfilled.

AITAH for telling my wife she needs to cover the cost of our daughter’s future?

As noted by financial psychologist Dr. Brad Klontz, author of ‘Money and a Relationship,’ financial issues often surface as proxies for deeper emotional needs and power struggles within a partnership. This situation exemplifies a breakdown in long-term financial alignment, rooted in an initial, perhaps emotionally charged, agreement made under different economic circumstances.

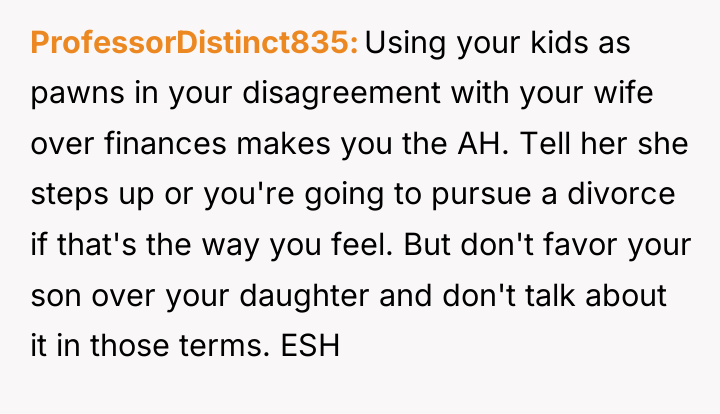

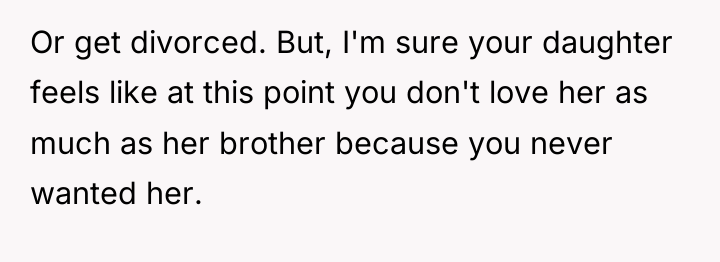

The husband’s motivations appear rooted in a strong sense of responsibility and perceived fairness, evidenced by his aggressive personal savings habits. However, his method of enforcing change—bringing up the original agreement years later, threatening divorce, and demanding immediate asset consolidation—is confrontational. The shift in the wife’s income from supplementary ($40k) to significant ($96k) fundamentally altered the financial reality they operate under, making the original agreement obsolete in practice. The threat of divorce and discussion of FASFA implications introduce significant adversarial components into what should be a collaborative family planning discussion.

The core conflict lies in differing views on shared marital assets versus personal earnings and differing perceptions of commitment. The husband views his contributions as overwhelmingly dominant and expects a corresponding level of shared future commitment, especially concerning the children’s education fund. A more constructive approach would involve transparent, non-confrontational financial planning sessions focused on the children’s college costs as a joint goal, rather than framing the wife’s previous agreement as a transactional debt. While the husband’s concern for fairness is valid, leveraging past agreements and threats undermines the trust necessary for joint financial governance.

THIS STORY SHOOK THE INTERNET – AND REDDITORS DIDN’T HOLD BACK.

The husband feels burdened by the disproportionate financial responsibility he carries for his children’s expected high-cost education, despite a past agreement where his wife accepted full financial responsibility for their second child’s extracurriculars. His current action is driven by a desire to enforce this original agreement and achieve perceived financial equity within the family unit for both children’s futures.

Given the husband’s extensive financial contributions and his insistence on pooling assets for equitable educational opportunities, is his ultimatum—demanding joint financial commitment for the children’s education or reverting to the original, limited agreement—a necessary step to enforce fairness, or does it represent a damaging breach of the established financial dynamic?

{kind=link}