In a world where family support often feels like a given, this individual faces a heartbreaking dilemma: burdened with a hidden debt they never agreed to, they wrestle with the weight of a parent-plus loan that shadows their newfound freedom. Despite having paid off their own student loans, the lingering financial obligation imposed by a parent’s secret borrowing feels like an unfair chain, especially when promises of support are broken.

Amidst this financial struggle lies a deeper, more painful rift—a clash of values and acceptance. As a proud gay adult finally embracing their truth, they face not only monetary hardship but also familial rejection, denied the very support their siblings receive for their weddings. This story is a powerful testament to the complexities of love, obligation, and the courage to stand firm in one’s identity against the odds.

WIBTA if I refuse to pay parent plus loans after coming out as gay?

As stated by financial therapist and author of ‘The Total Money Makeover,’ Dave Ramsey, regarding parental co-signing or debt: ‘When you co-sign, you are legally and financially tied to that debt. If the primary borrower defaults, you are on the hook.’ While this situation involves Parent PLUS loans (which are legally the parent’s debt unless refinanced), the underlying principle involves shared financial responsibility and expectation setting.

The core of this conflict rests on two major areas: implicit contract versus explicit agreement, and conditional vs. unconditional familial support. Parent PLUS loans are legally the parent’s responsibility. The OP’s feeling of obligation stems from the fact that the funds directly benefited their education, creating a perceived moral debt. However, this perception is severely undermined by the parents’ clear financial discrimination concerning the OP’s marriage due to their sexual orientation. This uneven distribution of financial support—funding the siblings’ weddings while refusing to reallocate loan payoff help for the OP—shifts the dynamic from unconditional parental support for education to conditional financial leverage.

The OP’s update shows a healthy recognition that separating the education debt from the emotional distress regarding the wedding funds is necessary for a clear path forward. The initial motivation (education) is distinct from the subsequent parental actions (withholding support based on sexual orientation). While the OP is certainly justified in feeling hurt and treated unfairly, a constructive recommendation is to confirm precisely how the $20,000 was used. If it was entirely for tuition, the OP should honor the commitment to repay the educational benefit, perhaps offering a structured repayment plan for the portion they feel responsible for, while simultaneously establishing firm boundaries regarding future financial or emotional support that is contingent on their personal life choices.

THIS STORY SHOOK THE INTERNET – AND REDDITORS DIDN’T HOLD BACK.

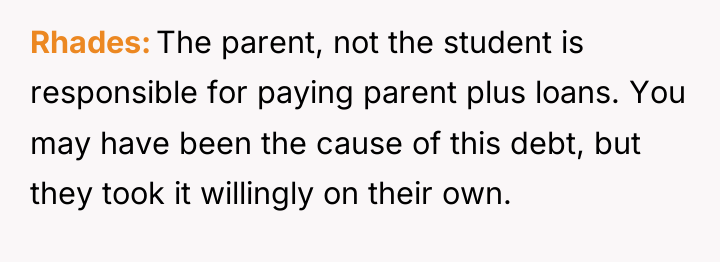

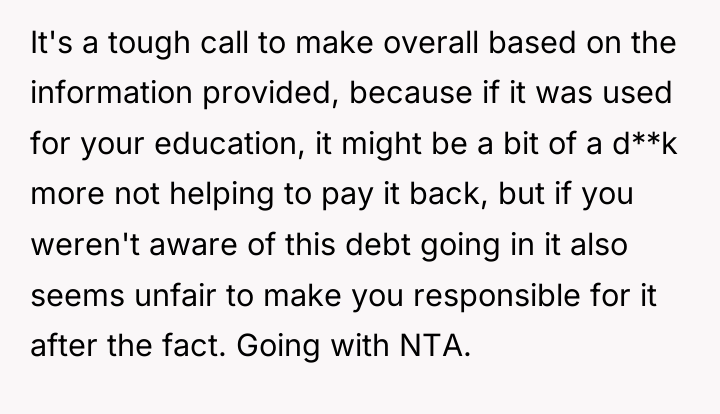

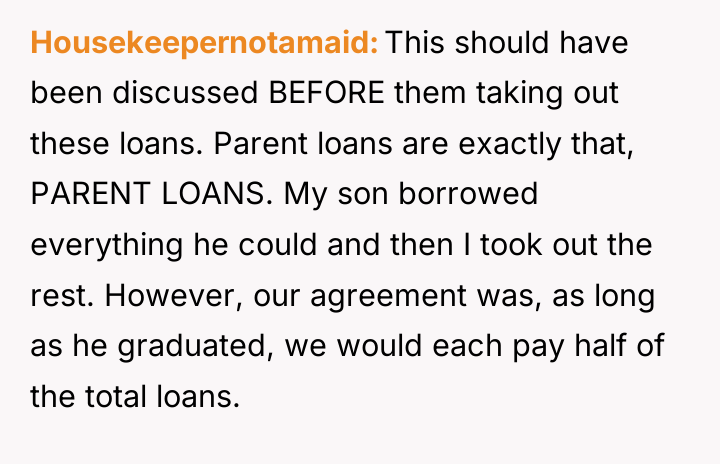

This should have been discussed BEFORE them taking out these loans. Parent loans are exactly that, PARENT LOANS. My son borrowed everything he could and then I took out the rest. However, our agreement was, as long as he graduated, we would each pay half of the total loans.

![[deleted] If you are in the US? It's the parent...](https://animalstrend.com/wp-content/uploads/wp-img-cache/638eb05a57033bd74fa8f1a8938605a8.png)

![[deleted] Info: I'm confused about this loan in that you...](https://animalstrend.com/wp-content/uploads/wp-img-cache/2ef6eac71f5d6cbf4fac3824df39eac1.png)

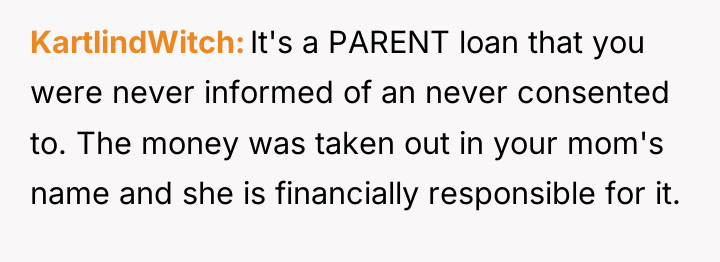

The individual in this situation feels a strong moral conflict regarding a significant debt taken out by their parent without their initial knowledge, especially when compared to financial support given to siblings for non-essential expenses.

Is the moral obligation to repay a Parent PLUS loan, taken out for education, nullified when the parents simultaneously withhold financial support for major life events (like marriage) based on personal moral objections, or does the foundational benefit of the education maintain the debtor’s responsibility regardless of parental inconsistency?

{kind=link}