A young woman secures a rare and highly advantageous bank loan, viewing it as a life-changing opportunity for her financial future.

However, her excitement is met with resistance from her boyfriend, who envisions a different path for their shared future.

AITAH for wanting to buy my own property now even though my boyfriend is against it because he wants us to buy one together, later on?

As financial expert Suze Orman emphasizes, ‘True financial freedom is the ability to live your life on your own terms.’ In this situation, the conflict arises from a fundamental difference in financial values and life planning. The OP views the loan as an asset that facilitates independence, while her partner perceives debt as a barrier to their collective goals. This divergence often reflects deeper power dynamics regarding how couples navigate individual versus shared agency early in a relationship.

The partner’s desire for the OP to reject the loan suggests a focus on mutual control rather than individual autonomy. When one party attempts to influence the other’s financial decisions based on a hypothetical future, it can create unnecessary resentment. The OP’s decision to accept the loan is objectively sound, as it leverages a rare professional opportunity. Moving forward, the OP should communicate that her financial security is non-negotiable and encourage her partner to focus on his own financial goals rather than attempting to direct hers.

AFTER THIS STORY DROPPED, REDDIT WENT INTO MELTDOWN MODE – CHECK OUT WHAT PEOPLE SAID.

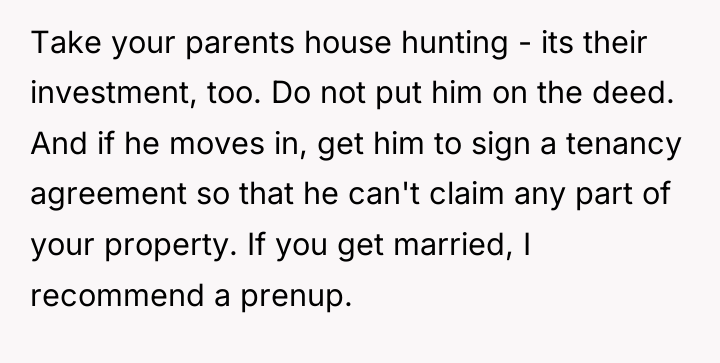

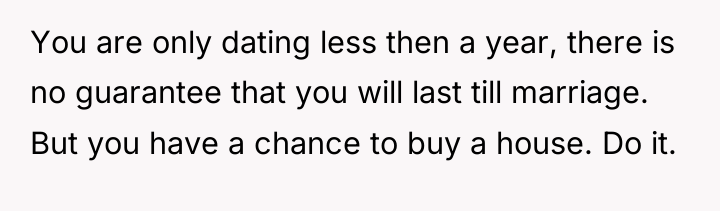

You aren’t engaged, so while you might be thinking about a future together, there isn’t any commitment at this point.

The OP prioritizes financial security and seizing a unique professional benefit, while her partner prioritizes total debt avoidance and independent joint homeownership.

The central question remains: Does the OP have the right to secure her own financial stability, or should she prioritize her partner’s vision for their life together?

{kind=link}