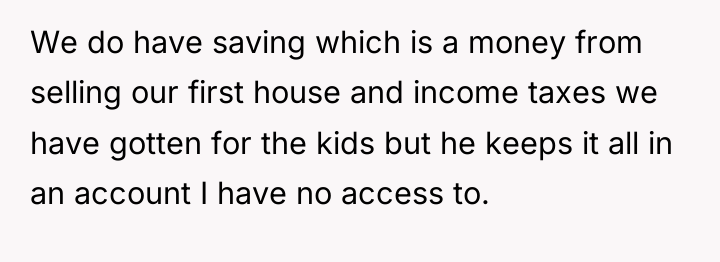

The user, a 30-year-old woman, has been in a long-term relationship with her 31-year-old husband since they were teenagers, and they now share four children. In 2021, the husband received a promotion and requested that she quit her casino job to become a stay-at-home mother (SAHM), promising he would cover all household bills.

Since quitting, her small work-from-home income was used mostly for their daughter’s competitive cheerleading, leaving her short for personal needs and gas. After losing that side job, she accumulated $1,700 in credit card debt, which he reluctantly paid. Now facing $2,500 in new debt accrued partly because he refused to help with the daughter’s cheer commitments, she is asking him for a weekly allowance and help with the debt, leading her to question if she is wrong to ask.

AITAH for asking my husband to pay off my debt.

In the field of relationship finance, Dr. Casey James is known for noting, “Financial control, even when disguised as protection or management, often becomes a significant source of relationship power imbalance and subsequent marital distress.” This situation highlights a classic dynamic where one partner holds the primary income and control over assets, leaving the other partner financially dependent without adequate resources for personal maintenance or agreed-upon responsibilities.

The husband’s behavior—asking the OP to leave employment, controlling all savings she has no access to, and refusing to fund necessary shared family activities (like cheerleading) while demanding she cover debts incurred partly due to those demands—suggests a lack of recognition for the value of her unpaid labor. While he covers base bills, the lack of any personal spending money ($200/week) or shared responsibility for agreed-upon child expenses forces the OP into debt, which undermines the security of the arrangement.

The OP is not wrong to request an allowance or debt assistance; these are reasonable requests for a full-time, long-term caregiver in a high-earning household. A constructive path forward requires establishing clear boundaries around personal autonomy, including a dedicated, accessible budget for the OP that acknowledges her contributions and covers necessary expenses related to the children. The current arrangement effectively treats her as an employee without a salary or expense account.

REDDIT USERS WERE STUNNED – YOU WON’T BELIEVE SOME OF THESE REACTIONS.

The original poster (OP) feels trapped in a financially restrictive situation where, despite managing the household and childcare full-time after being asked to leave her job, she has no personal income and is accumulating debt due to unmet needs, especially those related to the children’s activities. Her husband, who earns a high income, controls all shared savings and refuses to provide her with necessary personal funds or assist with the debt incurred under these circumstances.

The central question is whether the OP is entitled to a personal allowance and shared responsibility for the debt given her role as the primary caregiver, or if the husband’s complete financial provision for household bills fulfills all his obligations. Should the OP receive an agreed-upon personal budget, or is it reasonable for her to manage all non-bill expenses, including her children’s activities, solely on credit?

{kind=link}