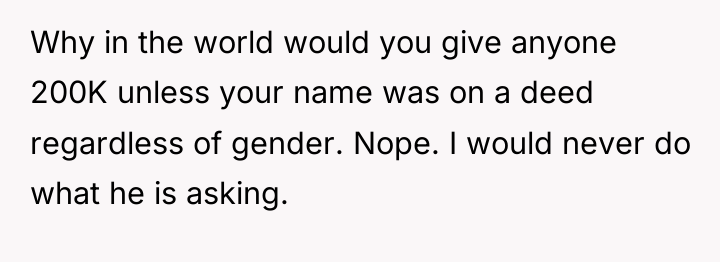

The original poster (OP), a 32-year-old woman, purchased her starter home at the age of 22. Her husband, 33, moved in three years later. Although the husband has never contributed to the mortgage payments, the couple is now planning to move to a larger house, driven primarily by the husband’s desire for a “man-cave,” a home office, and space for hosting parties.

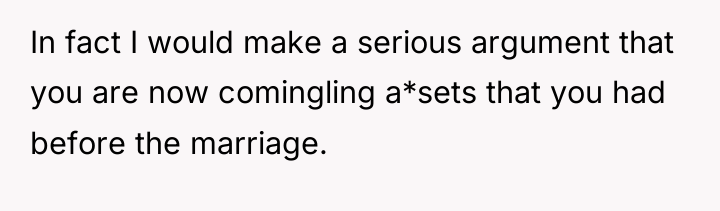

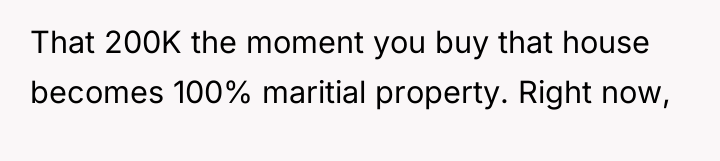

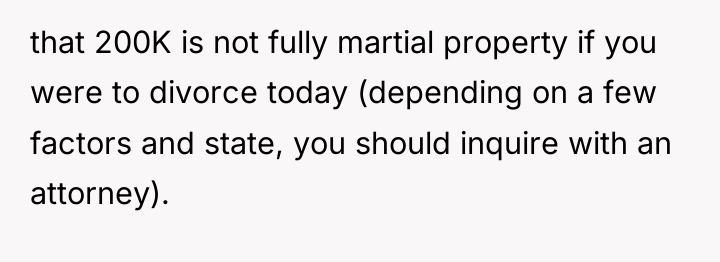

The core conflict arose when the husband insisted that only his name should appear on the deed of the new house, arguing he could use first-time homebuyer benefits to save on closing costs, while using the $200K equity from the current home (which OP bought) for the down payment. When the OP stated she required her name on the deed for protection, the husband became angry, suggested she seek therapy for her thinking, and dismissed her concerns as flawed. The OP is now facing a dilemma about proceeding with the move under these unequal financial terms.

AITAH for telling my husband I would not move without my name on the house

In the field of marital finance and asset protection, Dr. Dakota Kelly is known for noting, “When one partner treats shared marital equity as solely available capital for their individual benefit, it signals a fundamental imbalance in perceived partnership, regardless of past financial contributions.” This situation strongly reflects an issue of perceived fairness and boundary setting.

The OP’s concern is rooted in sound risk assessment. She bought the first home, and her husband’s suggestion to exclude her from the new deed, while using $200K of equity derived from her initial asset, suggests a desire for unilateral control over the most significant marital asset. His reaction—labeling her necessary self-protection as ‘flawed thinking’ requiring therapy—is a form of deflection, shifting responsibility for the conflict from his inequitable demand to her reaction to it. This pattern is concerning, especially considering his past financial rigidity (e.g., canceling her gym membership) contrasted with his significant personal desires (man-cave).

The move toward a larger home must be a mutual decision with mutual protection. The path forward requires the OP to stand firm on her non-negotiable stance. Any move that results in her utilizing her equity to acquire an asset solely in his name sets a dangerous precedent for future financial negotiations and security. A professional approach dictates that both names must be on the deed, or the equity contribution from the current home should be clearly defined as a loan rather than a gift toward his sole ownership.

AFTER THIS STORY DROPPED, REDDIT WENT INTO MELTDOWN MODE – CHECK OUT WHAT PEOPLE SAID.

The OP is positioned between supporting her husband’s desires for a larger home and firmly protecting her own financial security, especially given that she solely secured the initial property and holds significant equity. Her husband’s reaction—demanding sole ownership while utilizing shared assets and suggesting therapy for her caution—highlights a significant disconnect regarding financial partnership and trust in the relationship.

The central question remains whether the OP should sacrifice her legal stake in their shared future assets to accommodate her husband’s financial strategy, or if her demand for equal ownership on the new property is a necessary boundary for marital stability. Readers must weigh the value of financial self-preservation against maintaining marital harmony in this high-stakes purchase.

{kind=link}